For a second portion of Q2 “elephant eating”, I’ll look in some detail at the dynamics of an early instance of spot price volatility in Queensland, because many drivers turn out to be similar across other volatile intervals in the quarter.

Table Setting

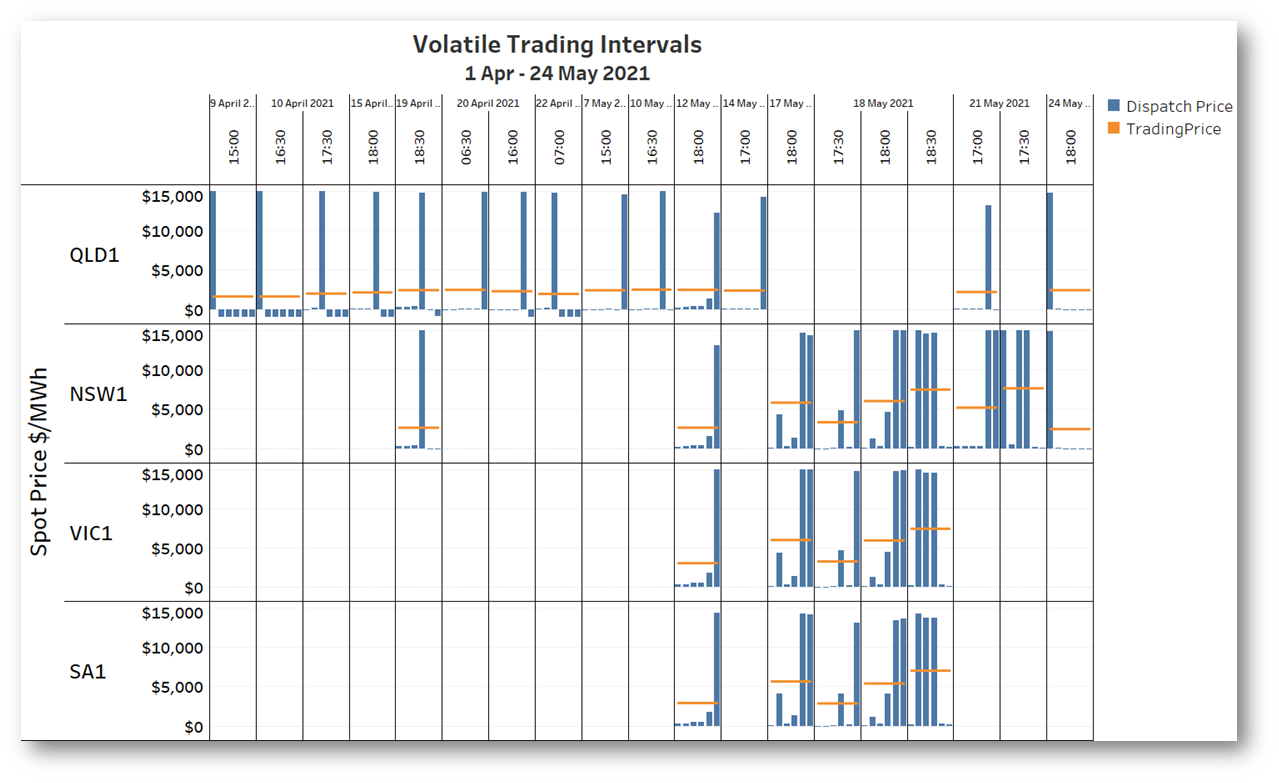

As context, the following chart shows trading intervals where one or more mainland regions saw at least one five-digit dispatch price, in the period prior to the Callide C generator failure. Both five minute dispatch prices and half hourly trading prices (average of six dispatch prices) are shown. For settlement, it’s the value of energy based on the trading price, not individual dispatch prices, that is paid by customers and received by generators.

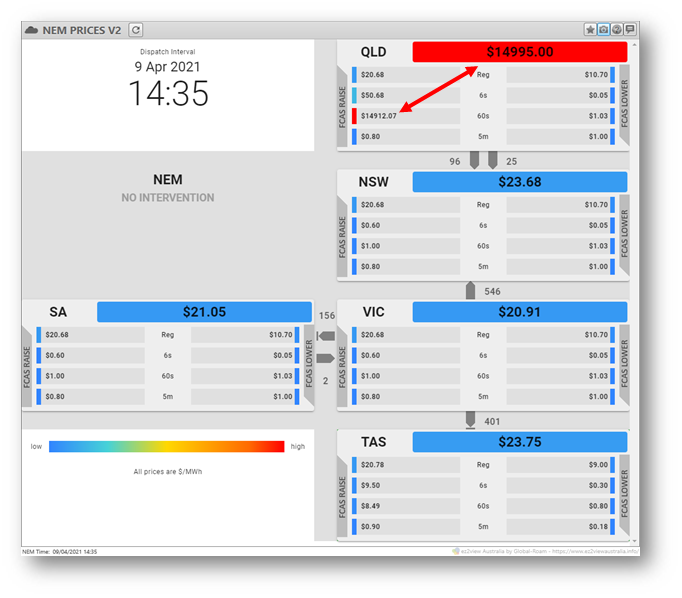

Early in the quarter, the majority of volatile intervals occurred in Queensland. I’ll be looking at the very first, the first dispatch interval in the half hour ending 15:00 on April 9.

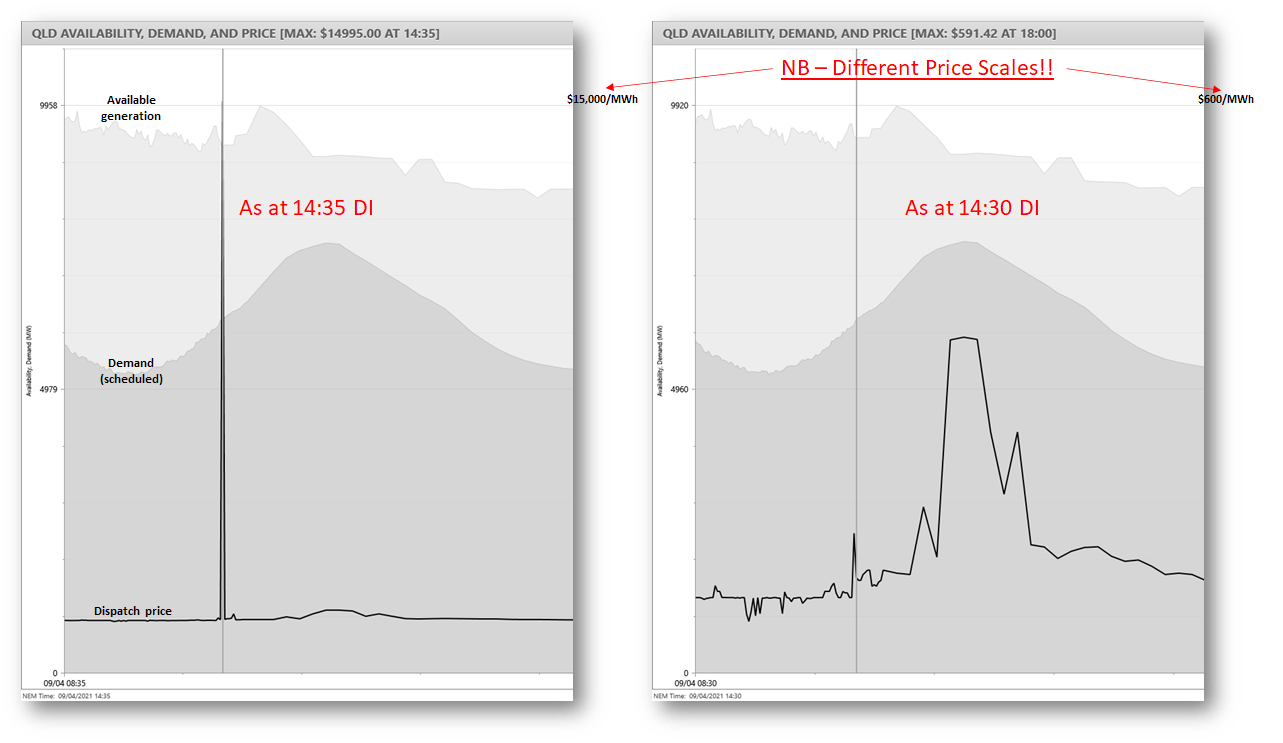

This pair of trend charts from ez2view shows the five minute price spike occurring in this interval (left panel), and the predispatch outlook seen in the immediately preceding interval (right panel). The spike to $14,995/MWh was not forecast by AEMO’s predispatch process.

There are many reasons for spikes like this not being forecast, even five minutes ahead; real-time measured inputs and constraint formulations in dispatch can vary significantly from those used in predispatch. Perhaps more surprising is price volatility appearing when the margin between demand (the darker grey area series) and available generation (light grey) seemed so comfortable.

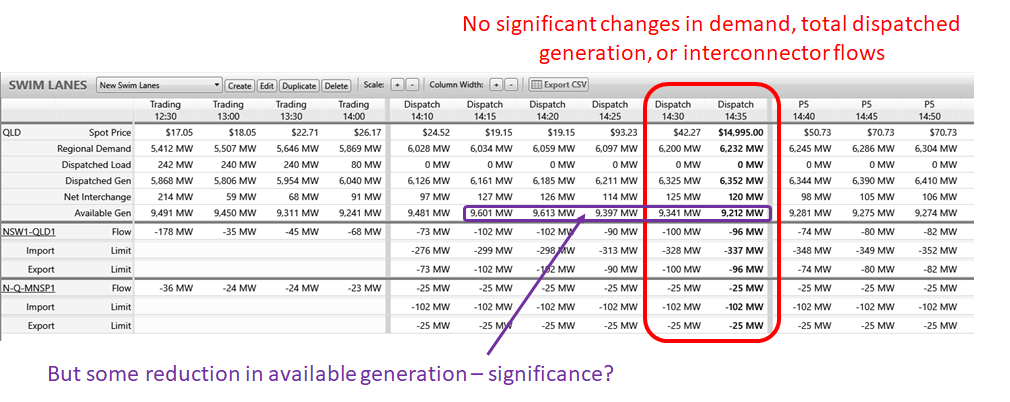

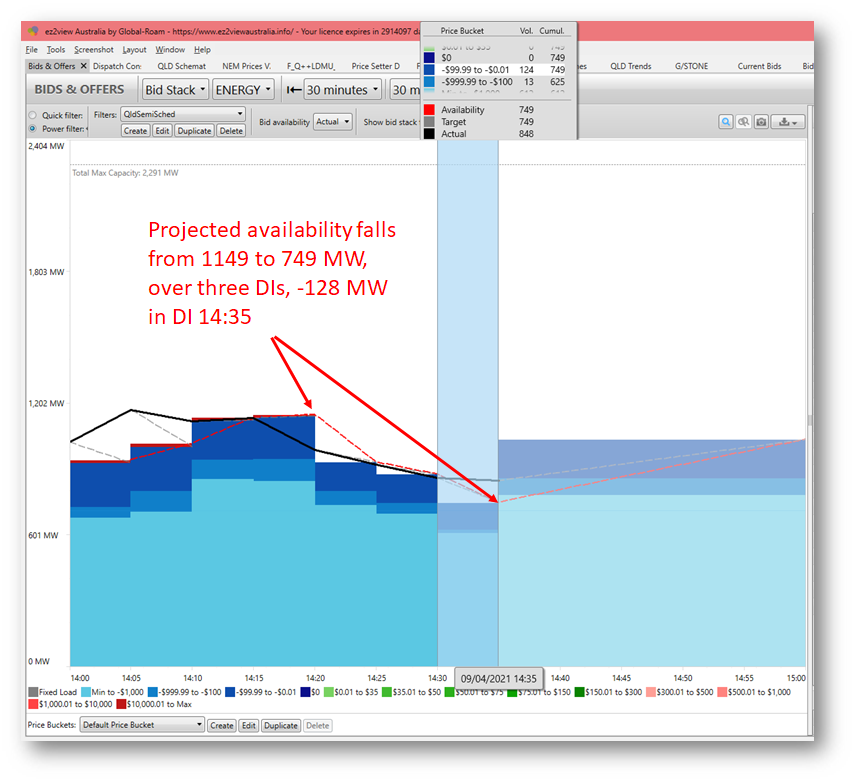

For those who prefer numbers to charts, ez2view’s ‘Swim Lanes’ view can tabulate time series for some of the high level dispatch quantities covering price, demand, generation, availability and interconnectors:

Apart from the leap in dispatch price the only change that stands out – sort of – is a relatively shallow short term downtrend in Available Generation, by about 400 MW over three dispatch intervals.

Diving In

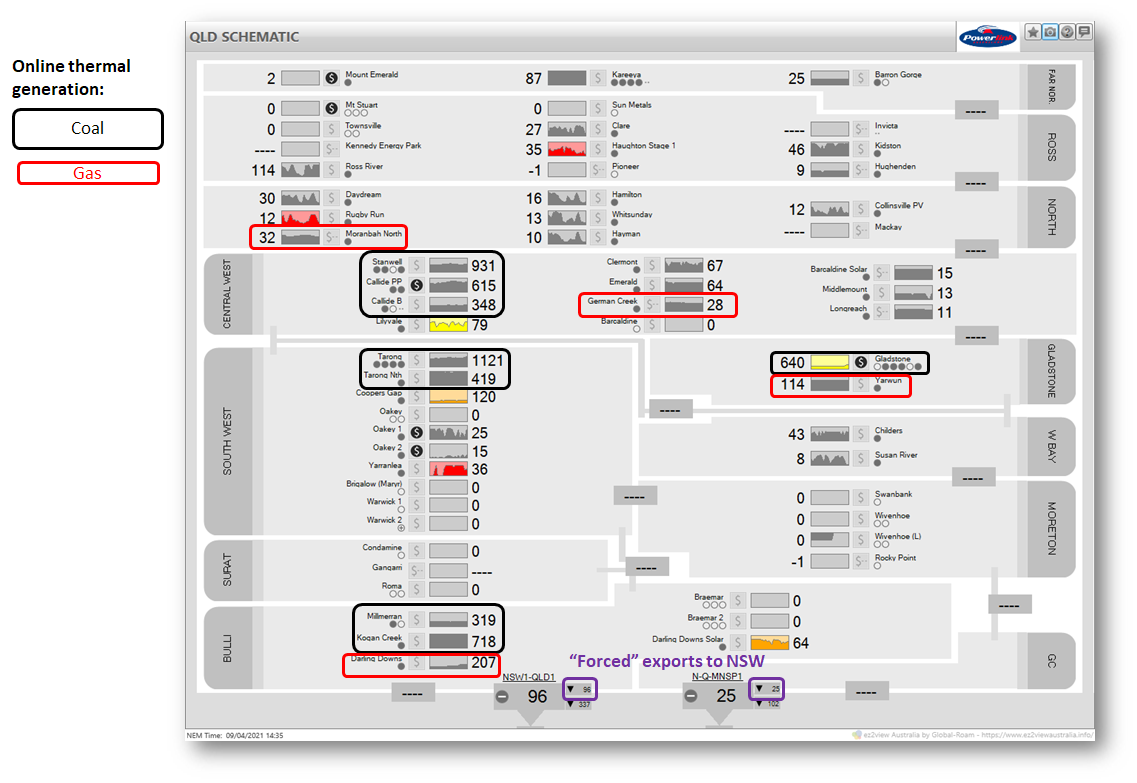

A schematic view of generation running in Queensland is helpful in understanding the prevailing dispatch pattern in more detail:

- Black coal-fired generation is the dominant supply source, totalling just over 5,100 MW. The number of offline units is typical for this time of year.

- Large scale renewables are providing just under 1,000 MW in aggregate, most of this solar. (Small scale rooftop PV does not show up in NEM dispatch as supply, but through reduced grid demand. At the time it was providing roughly 1,700 MW.) The capacity factor mini-charts for solar farms show significant fluctuations in output, suggesting that it was an afternoon of broken cloud cover.

- The only gas generation running was at Darling Downs, Yarwun, German Creek, and Moranbah, providing less than 400 MW in aggregate. None of these are higher cost “peaking” gas generators, as expected given the moderate prevailing demand and prices.

- Flows on the interconnectors with NSW were being “forced” south (indicated by both import and export limits being oriented towards NSW). This reflects operation of a constraint which I’ll discuss below.

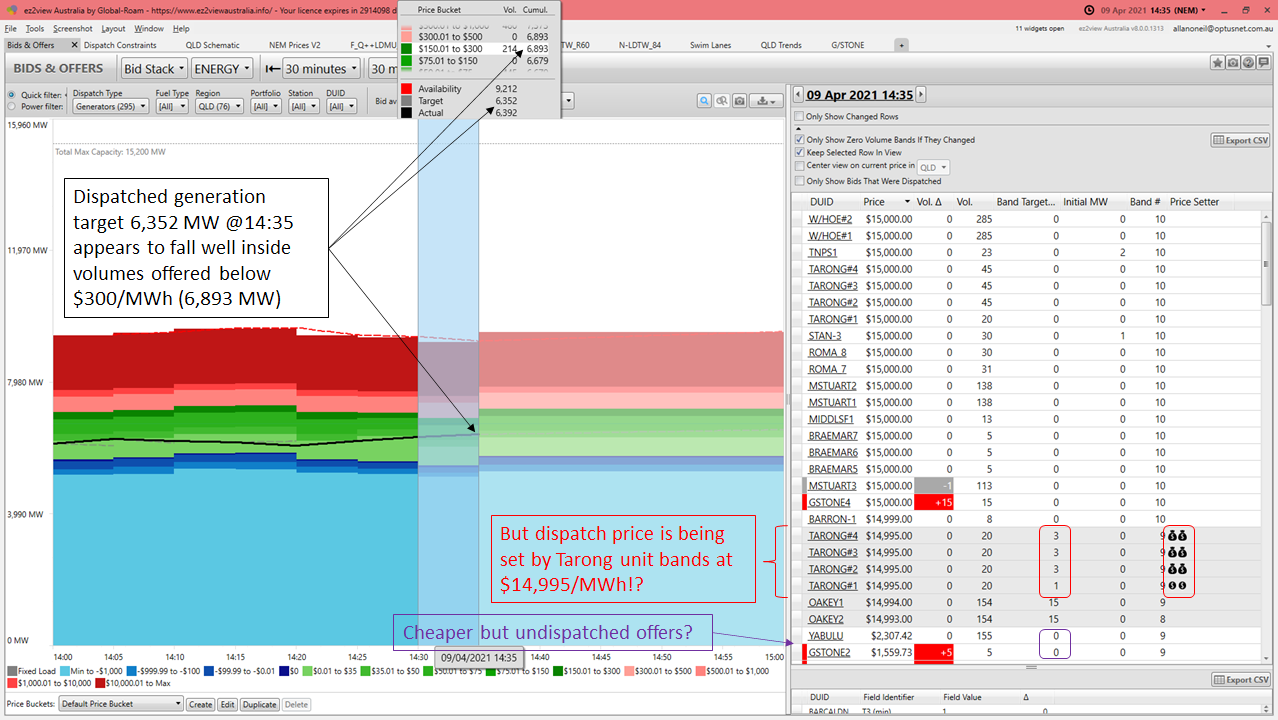

To unpick all this further, let’s look at supply offers in Queensland using ez2view’s Bids & Offers tool, adding a price dimension to supply volumes available.

This provides a LOT more detail about what was going on in this interval, but not necessarily more immediate insight. The aggregate dispatched generation target in Queensland appears to sit well within bands offered at low or moderate prices – the blue and green volumes on the chart – but the bid table shows offer bands from Tarong (coal) and Oakey (gas) units have been given non-zero dispatch targets, with the Tarong bands at $14,995/MWh setting the dispatch price. And just below the dispatched Oakey offers at $14,993 and $14,994/MWh, we can see a lower priced offer from Yabulu (Townsville gas turbine) with 155 MW apparently available but receiving a 0 MW dispatch target. And furthermore, despite the five digit price in Queensland, the region is exporting to NSW, requiring more expensive local generation to run, rather than importing cheaper supply from interstate. What’s going on?

Quite a lot. In summary I’ve found five main reasons for dispatch targets “skipping up the bidstack” to five digit territory, leaving on the table large undispatched volumes of cheaper offer bands and foregone interconnector imports from NSW. They are:

- Startup times

- Ramp rates

- Local FCAS requirements

- Interconnector / FCAS constraint interaction

- Semi-scheduled availability

In combination these are almost a mini-elephant in themselves, and all this only for one five minute dispatch interval. But let’s plow on and discuss them in turn.

Slow Off The Mark

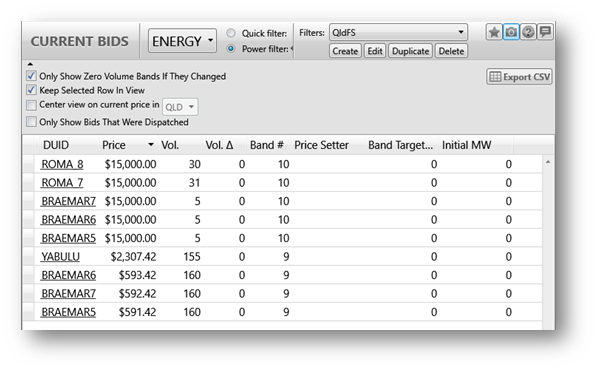

Below I’ve filtered offer data from ez2view for just a few of Queensland’s peaking generators for the 14:35 DI, including the Yabulu and Braemar units with offers priced well below the outturn dispatch price.

The zeroes in the InitialMW column show that none of these units were producing energy at the start of the dispatch interval. And despite some of their offer prices being below those of the Tarong bands that set the price, their end-of-interval dispatch targets remained at zero.

The reason for this is that generators which choose to offer as “fast-start” units must specify a minimum startup time and are handled in a very specific way by the NEMDE dispatch algorithm. In effect, operators of these units hand over to NEMDE their decisions on whether to start, and their startup output profile. If a fast start unit is not running at the start of a dispatch interval, but has volume in an offer band priced low enough to be dispatched based on economic merit, NEMDE follows a special series of steps:

- The unit receives a start signal

- If the unit’s specified startup time is under five minutes, NEMDE will give the unit a non-zero end-of-interval dispatch target based on that startup time, the unit’s minimum loading level, its offered ramp rate (see below), and possibly the overall generation dispatch requirement.

- If the unit’s startup time is longer than 5 minutes, the unit will get a zero end of interval target but will be scheduled by NEMDE to produce energy in a subsequent dispatch interval once it has started, consistent with its specified startup time and other parameters. So a unit with a 10 minute startup time will not be scheduled to actually produce energy until the third dispatch interval from startup (even though the spot price in that future interval may end up being quite different and perhaps lower than the unit’s offer price – NEMDE does not project prices forward but uses only the current dispatch price to determine startup).

In most of these cases, the fast start unit will not set the dispatch price, because its end-of-interval loading, whether zero or not, is inflexible – effectively hard-wired by its fast start profile parameters. There is significant additional complexity to the handling of fast start units in NEM dispatch, but that’s enough to know for our purposes here.

The Braemar and Yabulu units in the tabulation above had specified startup times of six and ten minutes respectively, so while they would have received start signals at the beginning of DI 14:35, they were not scheduled to produce any energy in that interval and did not contribute to price-setting.

The key takeaway here is that most of the “available” volume offered by offline fast-start units is not actually available within a single dispatch interval.

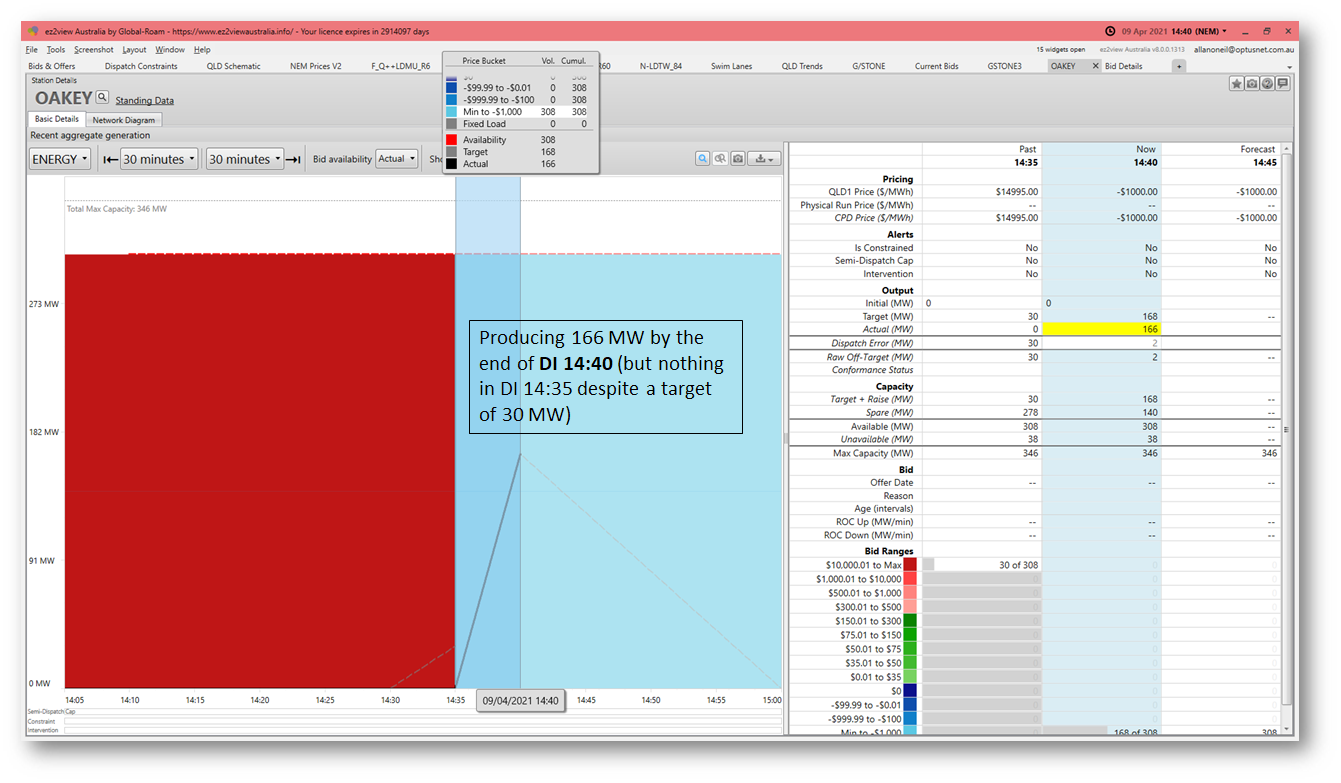

But what about the Oakey gas turbine units that received non-zero targets for their offers at $14,993 and $14,994/MWh – had they specified a shorter startup time?

In fact those units didn’t offer as “fast-start” units at all, even though within ten minutes – two dispatch intervals – they had ramped up to over 50% of their capacity:

These units offered as “self-committed” (or, confusingly, “slow start”) plant where the operator decides when to start and synchronise its generation but should do so in accordance with its bid volumes and dispatch instructions from NEMDE. The operator of the Oakey units appears to manage this by offering a low ramp rate of 3 MW/minute when offline, meaning that they can be scheduled for no more than 15 MW output if not producing at commencement of a five minute dispatch interval. Once dispatched, these units are typically rebid with much higher ramp rates in order to quickly move to higher output levels in subsequent DIs, as evident in the chart above.

Readers with a keen appetite for detail will notice that Oakey wasn’t actually producing any output at the end of DI 14:35 despite its scheduled target of 30 MW. Whether this is a glitch in startup, or for some other reason, isn’t clear.

Slow to React

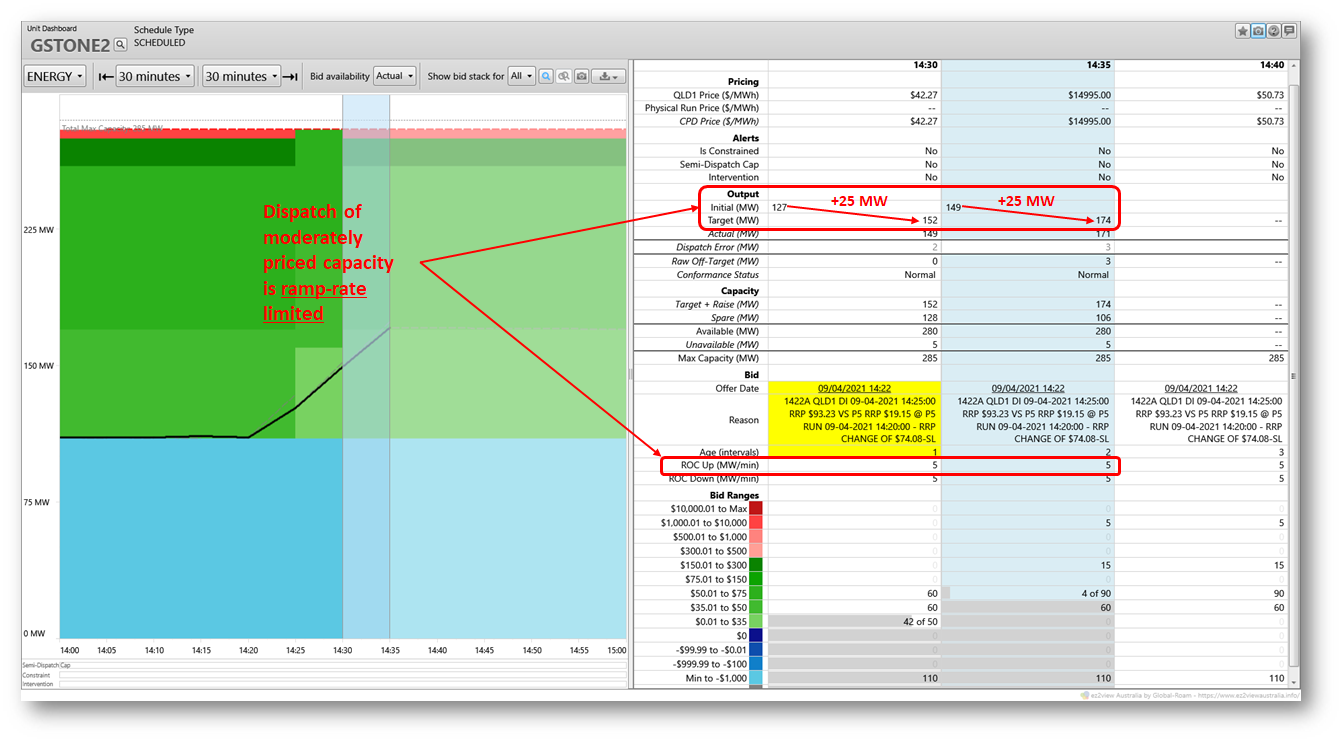

This brings us to true “slow start” units such as coal plant. As well as requiring hours for startup from offline, these units are often limited in how rapidly they can move between output targets. So, like offline fast-start plant, their effective availability within a single DI can be much less than apparent. As a single example of this in the DI we’re examining, here’s the dispatch of Gladstone unit 2:

At the start of the 14:35 MW DI the unit was producing 149 MW and had another 126 MW of capacity offered at prices below $300/MWh, but only 25 MW of this relatively low-priced “available” capacity could accessed in this DI due to its 5 MW/minute ramp rate limit.

Offered ramp rates do not always reflect actual physical capabilities. There is no reason to think that the 5 MW/minute ramp rate offered for this Gladstone unit is significantly different from its technical limits, but there are certainly instances in the NEM where participants vary ramp rate limits for economic reasons, adding another dimension to bidding strategies.

Keeping it Local

Often hidden from view in analysis of energy market dispatch is the parallel and “co-optimised” dispatch of FCAS – Frequency Control Ancillary Services. Across the entire NEM the required volumes of these services (very simply, capability of generators and loads to move their output and consumption in response to frequency deviations) are far smaller than energy volumes, and in general they can be procured from wherever in the NEM they are offered most inexpensively.

However there can sometimes be requirements for some FCAS volumes to be procured specifically in a particular region or group of regions, particularly if there are outages to key transmission lines. If FCAS volumes required from a specific region are large enough in proportion to the region’s energy generation, and particularly if there is a limited set of FCAS providers, this can have a substantial effect on energy market dispatch and prices, as well as on FCAS prices.

In the DI we’re examining, this was the siutation for a number of FCAS services. A planned transmission line outage in NSW required that significant FCAS contingency services had to be provided from Queensland suppliers to ensure system security.

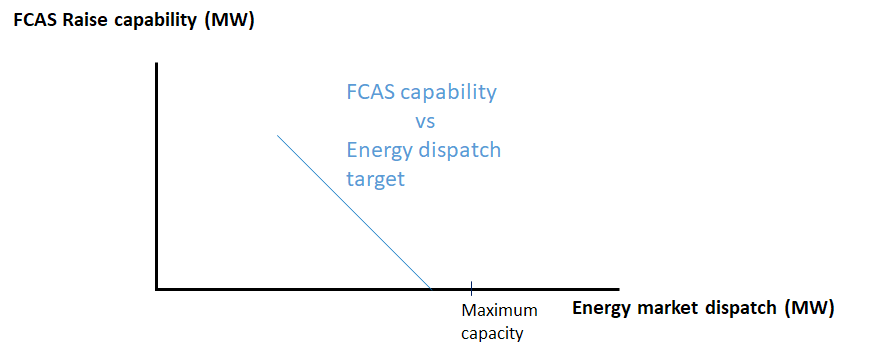

The issue arising is that the capability of generators to provide FCAS services can vary with their energy output. To provide “raise” contingency services which require increasing output in a rapid but controlled way if system frequency falls, most generators need to be operating below maximum output – if they’re dispatched at maximum in the energy market, their ability to increase output further has all been used up, so they have no “raise” capability available. In fact this capability may fall to zero at levels lower than maximum energy output, depending on generation technology.

We can capture this concept graphically quite simply:

The blue line represents a physical trade-off between higher energy market dispatch (unit output) and reduced FCAS Raise capability. For an FCAS Lower service, requiring reductions in output if frequency rises, we’d expect a reversed curve with increasing FCAS Lower quantities available as unit output increases from some level at or above minimum stable load.

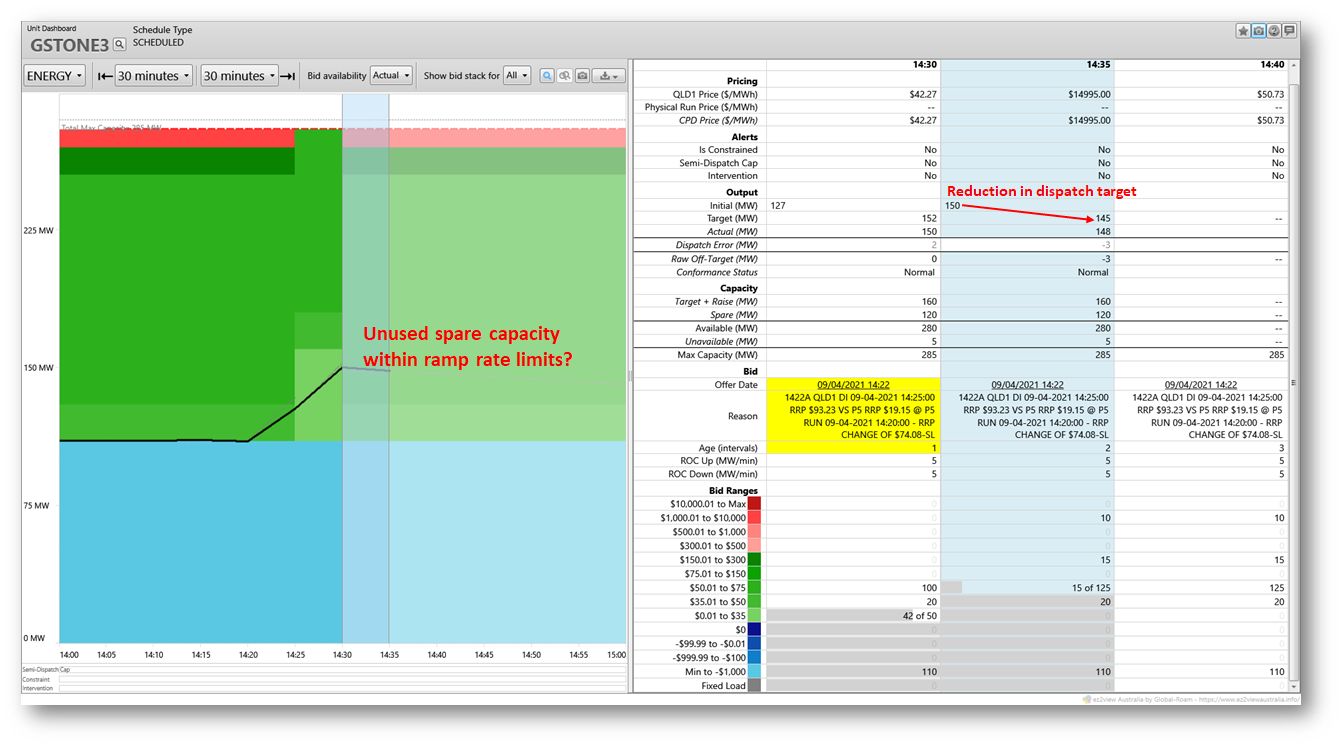

Without ploughing into the innards of “FCAS trapezia” and other complications, that insight should be enough to explain why some lower-priced available energy could not be dispatched from certain Queensland generators for the DI in question: the FCAS Raise quantities required from those generators meant that their dispatch in the energy market had to be limited. As an example, here’s dispatch for Gladstone unit 3:

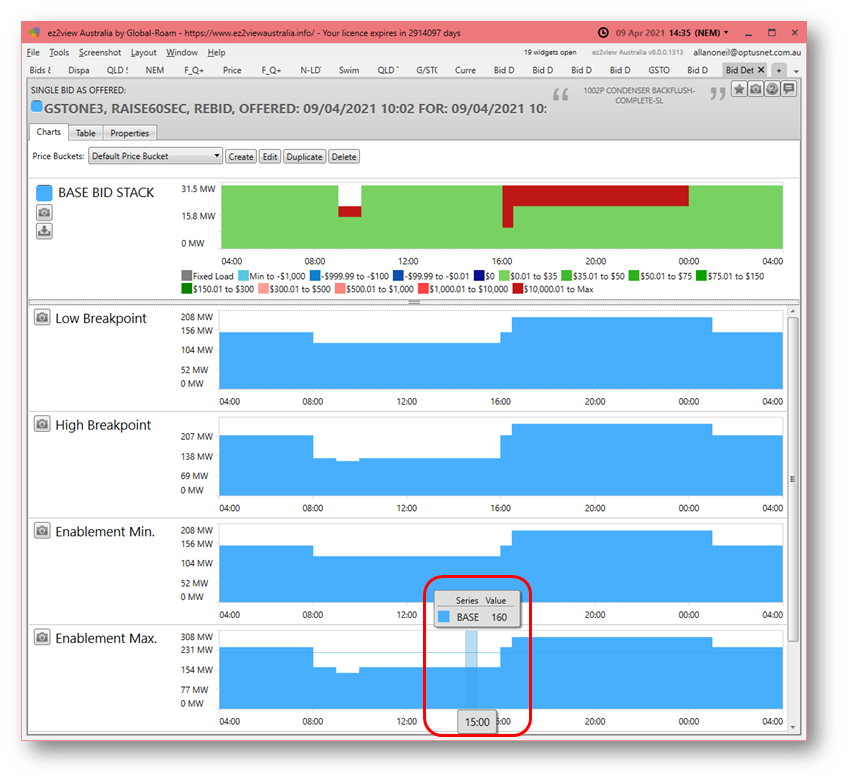

In DI 14:35 its energy dispatch target actually fell, despite plenty of remaining low price capacity being offered. It’s not obvious from this chart why this happened, but – without going into the full detail – the unit’s offer for the “Raise 60 second” FCAS service specified that it could only be enabled for FCAS when dispatched below 160 MW in the energy market (the “Enablement Max.” parameter in its FCAS offer below):

To provide its full offered volume of 30 MW for this raise service it would need to be dispatched at or below 130 MW.

So, even though Gladstone 3 was offering 285 MW of available capacity in the energy market, 125 MW of that capacity could not be accessed if the unit was required to provide any of this particular FCAS service – which it was for this DI, given the magnitude of local FCAS requirements in Queensland and a limited number of suppliers.

Replicate this across a number of different generating units and it can be seen that many hundreds of megawatts of “available” energy may not be available at all when FCAS raise services are in short supply.

A Vicious Circle

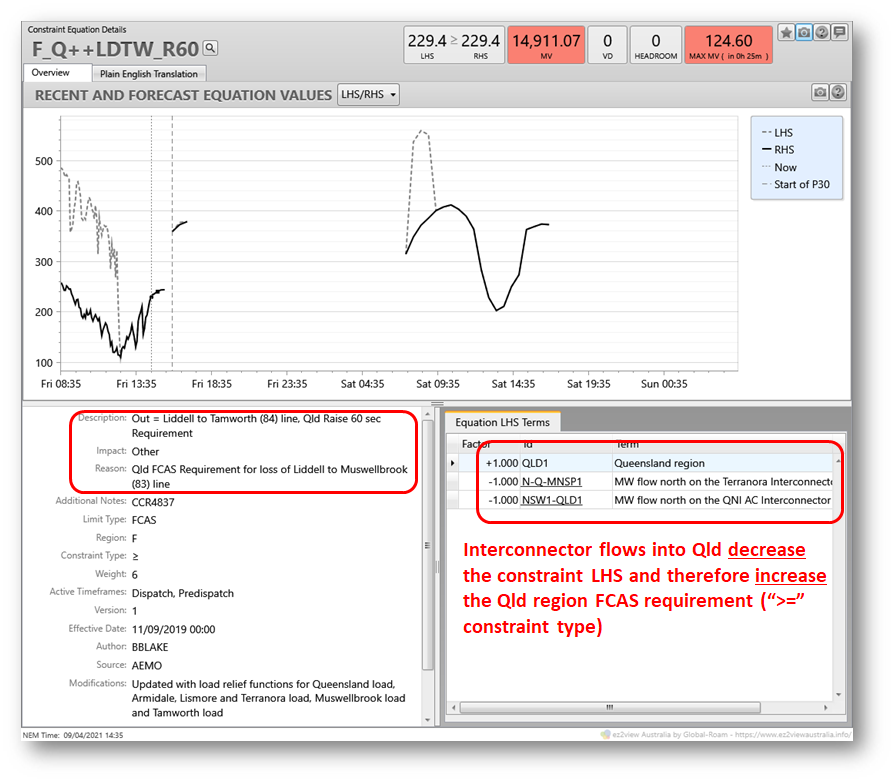

A related factor amplified the impact of the local FCAS requirement discussed above: the location of the relevant transmission line outage in NSW meant that any increase in energy flows from NSW generators northward into far northern NSW and Queensland would also increase the required volume of Queensland FCAS services – megawatt for megawatt. We can see this from the formulation of the constraint impacting Raise 60 second FCAS:

I’ve written other WattClarity articles on constraints explaining what all this means, but the key point is that trying to lower the dispatch of expensive energy offers in Queensland by importing from NSW – NEMDE’s normal strategy for minimising dispatch costs – wouldn’t work in this case because it would increase the amount of scarce Queensland FCAS capability needing to be procured. And as we saw above, doing this would reduce the dispatch of relatively cheap energy in Queensland in order to provide the necessary FCAS headroom – a nearly perfect vicious circle!

In the event, the solution found by NEMDE involved exporting expensive energy from Queensland into lower-priced NSW, simply to lessen the requirement for Raise 60 second FCAS to a level that could actually be procured from Queensland suppliers.

And if you have a feel for what co-optimised dispatch means, it won’t surprise you at all to learn that in this DI, the price of Raise 60 second FCAS therefore jumped to over $14,900/MWh:

Under a Cloud

Finally, what about renewables – did their behaviour have an impact? If we look at offers, availability and output from large scale Queensland renewables using ez2view’s Bids & Offers tool we can get a quick sense:

Clearly actual and expected aggregate and expected output from large scale renewable generators was declining going into DI 14:35. The projected step down of 128 MW over that DI would have correspondingly increased the dispatch required from other scheduled generators, but in terms of price outcomes this is probably just the “straw that broke the camel’s (elephant’s?) back” rather than a major factor. Conditions for price volatility arose more from the other factors discussed above than this specific cause.

(Note that although actual renewable output over the DI barely fell (black line on the chart), it’s the projected output that is used in dispatch and pricing.)

What to Follow?

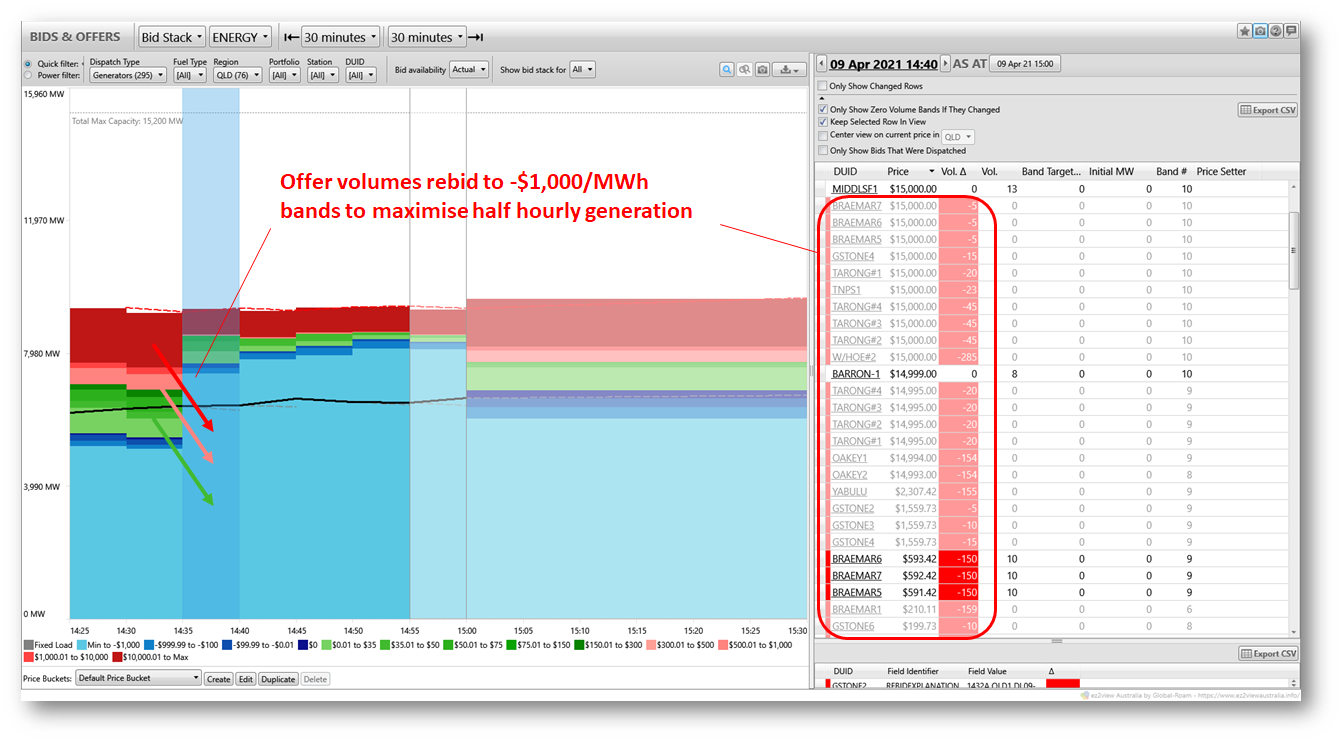

I’d be remiss not to quickly cover the balance of the half-hour trading interval (TI 15:00). What followed should be familiar to anyone who’s heard of the NEM’s “5/30 issue”. After the spike in the first dispatch price of the trading interval, multiple generators rapidly rebid volumes to their -$1,000/MWh offer bands in order to maximise generation within the half hour.

As shown in the very first chart of dispatch and trading prices, this resulted in negative prices for the balance of the half hour, but a still-elevated half hourly trading price of $1,666/MWh.

To Finish

It would clearly be a ridiculous exercise to descend into this level of analysis for every price spike in Q2 – a forensic dissection of the elephant’s toenails. But I think I can justify serving up the above because the same factors discussed in this post applied to many of the other volatility events seen over the quarter. Perhaps a reasonable question is why they didn’t lead to even more regular volatility.

It’s also a good reminder that price volatility in the NEM is often driven by many factors other than apparent supply-demand balance or simple reserve margin assessments. There are many more detailed drivers and behavioural factors lying behind periods of volatility.

Some of these factors are also very relevant to issues that will continue to arise as the NEM’s inexorable transition continues. Ramping capabilities, the role of not-so-fast-start plant in a five minute settled market, needs for FCAS, the interaction between transmission and the energy market, better forecasting of variable renewables. I could go on but that’s a big menu already.

In later posts I’ll perhaps try to address more of these issues and look further at some behavioural questions around bidding by different market participants, but I think I’ve already consumed more than enough of the elephant for this sitting.

About our Guest Author

|

Allan O’Neil has worked in Australia’s wholesale energy markets since their creation in the mid-1990’s, in trading, risk management, forecasting and analytical roles with major NEM electricity and gas retail and generation companies.

He is now an independent energy markets consultant, working with clients on projects across a spectrum of wholesale, retail, electricity and gas issues. You can view Allan’s LinkedIn profile here. Allan will be sporadically reviewing market events here on WattClarity Allan has also begun providing an on-site educational service covering how spot prices are set in the NEM, and other important aspects of the physical electricity market – further details here. |

Thanks Allan for dissecting the elephant’s toe nails. This consumer advocate found it fascinating since 5 minute settlement is rapidly approaching. Volatility in wholesale prices can flow through to retail power bills. Since QEUN’s April 2021 survey of over 200 businesses in the Cairns region found over 60% had a medium concern about the payment of their power bills (20% had a very large concern), then are consumers already struggling with power bills about to struggle with fluctuating power bills caused by volatile wholesale market?

Fair question Jennifer. As you know wholesale energy costs are a proportion of consumer bills, and that proportion depends quite a bit on location (network costs), customer size, retail on-costs etc. Most customers won’t be directly exposed to short-term spot market volatility but trends in wholesale prices flow through to forward contracts and to retail pricing with a time lag – the length of this lag can be quite appreciable, again depending on customer specifics. The first post in this little series (https://wattclarity.com.au/articles/2021/06/eating-the-nems-q2-elephant-an-appetizer/) has some views of the impact of recent volatility on average and forward contract prices. For Queensland, average and forward prices are now well above where they were six or even twelve months ago, but still well below the levels prevailing over most of 2017 – 2019. The energy price component of consumer bills for many customers, eg those on tariffs set ~12 months ago would still reflect some impact of the high prices prevailing in that period so I don’t think the current volatility by itself should lead to a *jump* in that component, but obviously if it extends into subsequent quarters that could change. What’s probable is that is that signficant falls in that component which seemed on the cards just a few months ago are now less likely.

Thanks Allan. If volatility increases then this could be priced into retail offers which could be more problematic for small retailers with small generation portfolios, this could impact retail competition. With the COVID19 pandemic continuing and no real idea as to when the international border will open, many businesses who are at present benefiting from lower wholesale/retail prices will have little ability to suddenly pay more if volatility is priced into retail offers in the future. Volatility is also enhanced by Jurisdictional Scheme Charges – a significant charge (eg 3.5%) that can without warning be imposed on consumers’ power bills. The COVID19 recovery of small business – the largest employer in Australia – is fragile eg Reserve Bank of Australia’s May 2021 charts has lending to small business as flat lining and business investment is continuing to fall despite the extension of generous tax write-offs (agriculture is bucking the trend). Therefore downward wholesale/retail prices are most welcome but a sudden spike or a consistent rise in wholesale prices would impede the COVID19 recovery. Since energy costs to over 700,000 business and residential customers in regional Queensland represent 35% of a power bill and 75% of the energy cost is the wholesale price, we are very interested to see if 5 minute settlement will increase volatility and therefore be priced into retail offers.