The NEM is rarely in the headlines for benign reasons these days, and leading up to a long-deferred COAG Energy Council meeting on Friday, a raft of articles have (re)appeared concerning risks to supply reliability as we approach the official start of summer.

We’ve covered this topic in a series of articles here on WattClarity, going back to June when we first looked at the impacts of major outages at Loy Yang A and Mortlake power stations and what these might mean for summer reliability. We then went into some depth covering AEMO’s outlook for reliability more generally, as published in the August Electricity Statement of Opportunities (ESOO).

Given the renewed media interest and the early arrival in most NEM states of weather more associated with peak summer conditions, it seems like a good idea to look at what if anything has changed since those earlier assessments.

ESOO Recap

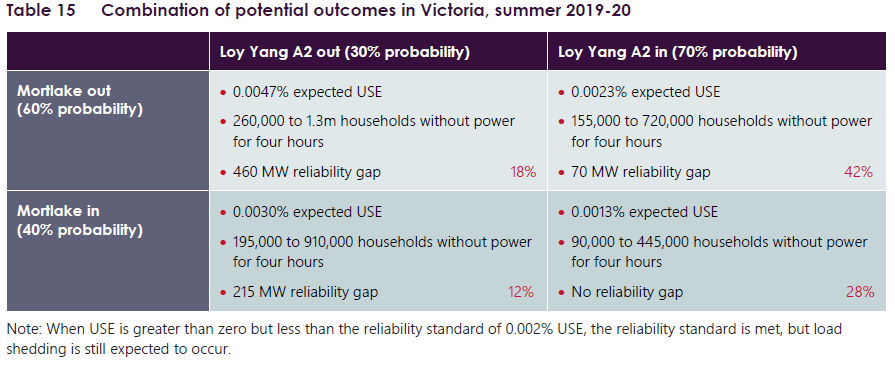

The ESOO identified Victoria as facing a higher probability of supply shortfalls this summer than other states, and the only region where the NEM’s formal reliability standard, based on “expected Unserved Energy (USE)”, was not forecast to be met. This was the direct result of the major Loy Yang A and Mortlake outages, and AEMO provided the following table summarising its risk assessment for Victoria under the four different scenarios where each of these units is either back in service or still being repaired over the peak summer period (formally January – March, although high temperatures and tight supply could of course appear at any time from now):

I’m not going to fully decode this table here, having previously commented on what the terms really mean (and how they could have been better communicated). But the key points are that, back in August:

- Although owners AGL and Origin Energy had indicated that the two units being repaired were scheduled to be back online in December, AEMO judged based on past experience that the risks of significant delays were material (30% for Loy Yang A2 and 60% for Mortlake).

- Under each combination of outcomes for on time versus significantly delayed return for the two units, different levels of reliability risk would result, summarised in the four quadrants. It’s worth re-emphasising that the “numbers of households without power” are NOT definitive predictions of blackouts but just AEMO’s way of trying to convey the relative size of shortfalls that might occur under an adverse combination of high demands and additional generation outages.

- The relative probabilities of each scenario, given AEMO’s assessment of delay risks, were indicated by the red percentages in each box.

- AEMO’s overall (dare I say “headline”) assessment of Victorian reliability concluding that the reliability standard was not satisfied, was based on a weighted average of data from the four quadrants, using these probabilities.

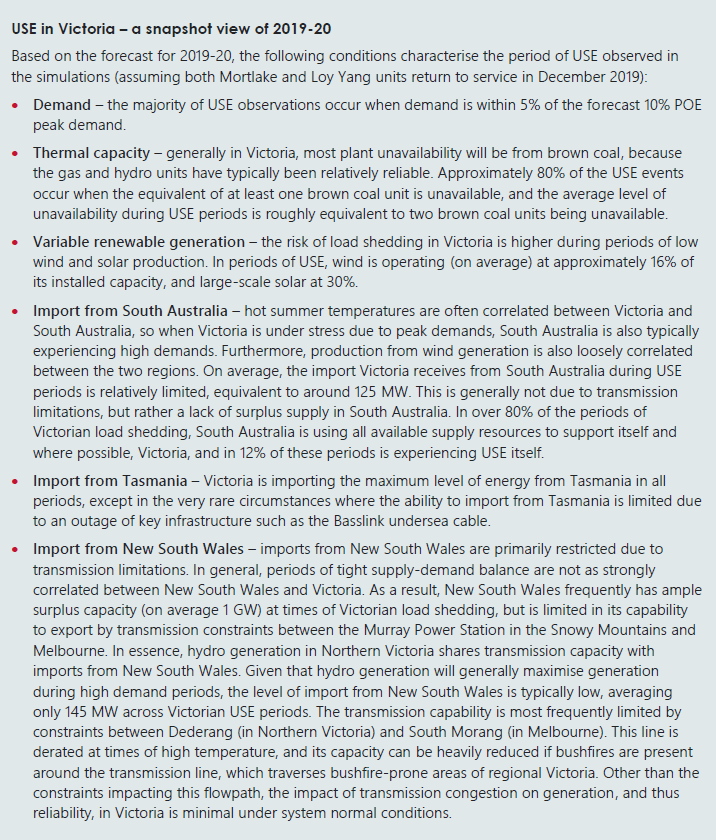

AEMO also a provided a very useful qualitative description of conditions under which Victorian supply shortages might emerge, based on insights from the literally hundreds of Monte-Carlo modelling runs that underlay its summary assessments. It’s worth reading if only to understand the many moving pieces in the reliability puzzle:

What, if anything, has changed?

We’re now three months on from the ESOO, so is there any new information on the key drivers for AEMO’s ESOO assessment – especially news on the all-important repair jobs being undertaken by AGL and Origin?

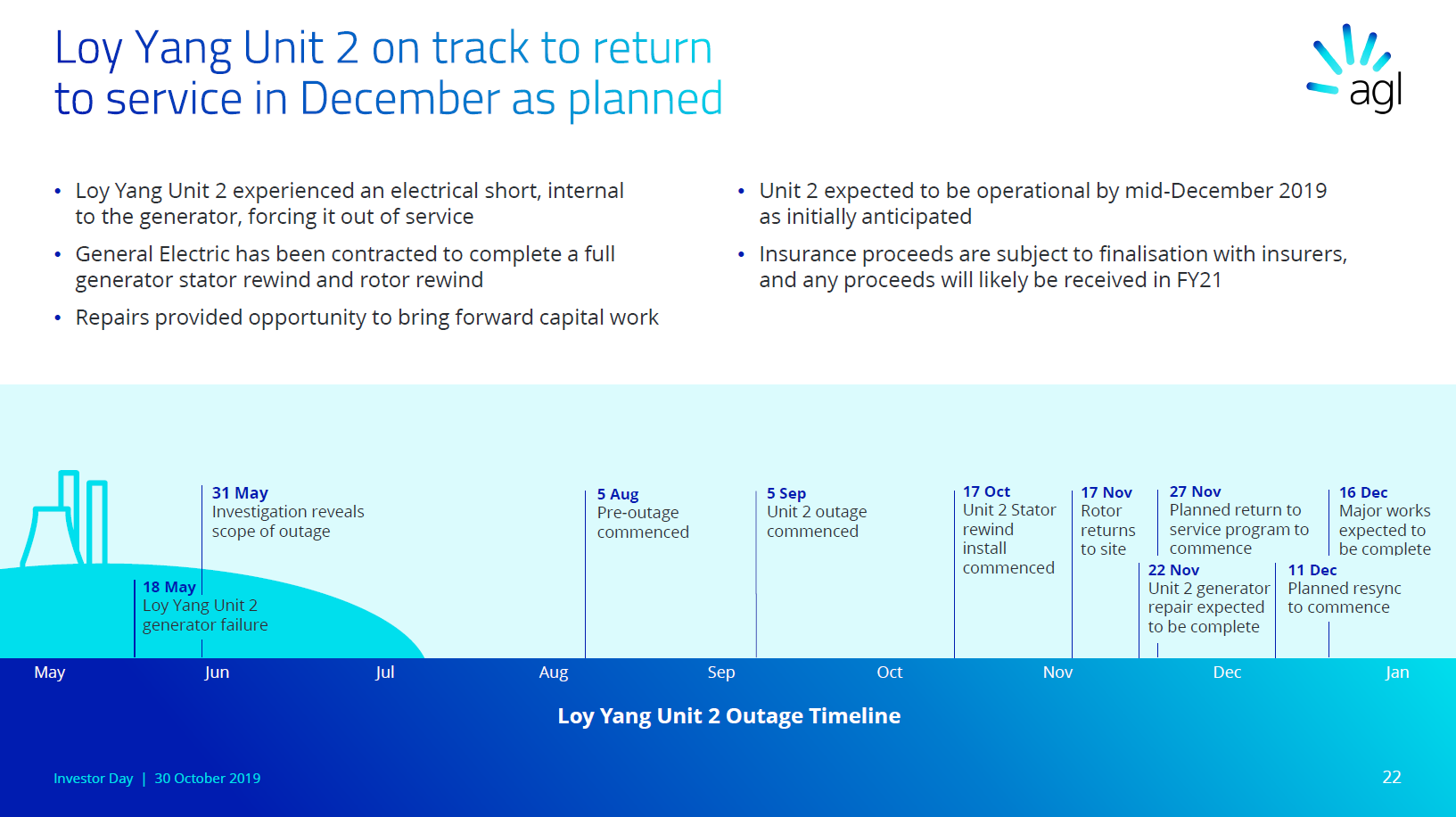

Loy Yang A2 (530 MW)

AGL produced a quite detailed outline of progress on this repair as part of its recent Investor Day presentation:

All seems to be on schedule which is good news, but it has to be emphasised that large and complex thermal generating units returning from major long term outages don’t necessarily perform to full capability the moment they come back online. It would not be surprising if there was a period of some weeks where testing and shaking out any bugs took place.

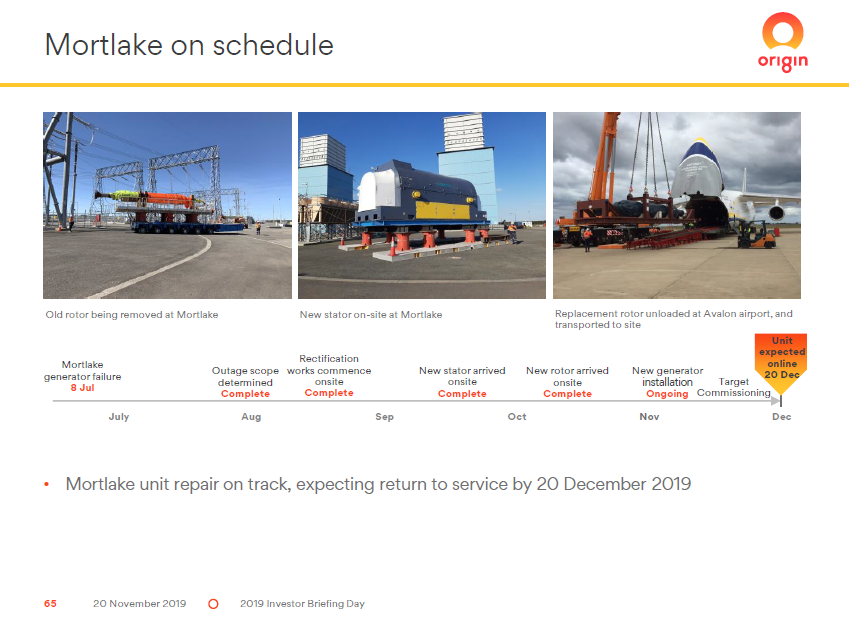

Mortlake Unit 2 (283 MW)

Origin followed AGL’s lead in its own investor day presentation this Wednesday, indicating that repairs are on schedule for a late December return:

Similar caveats about generators returning from long term outages obviously apply here too.

Other generators

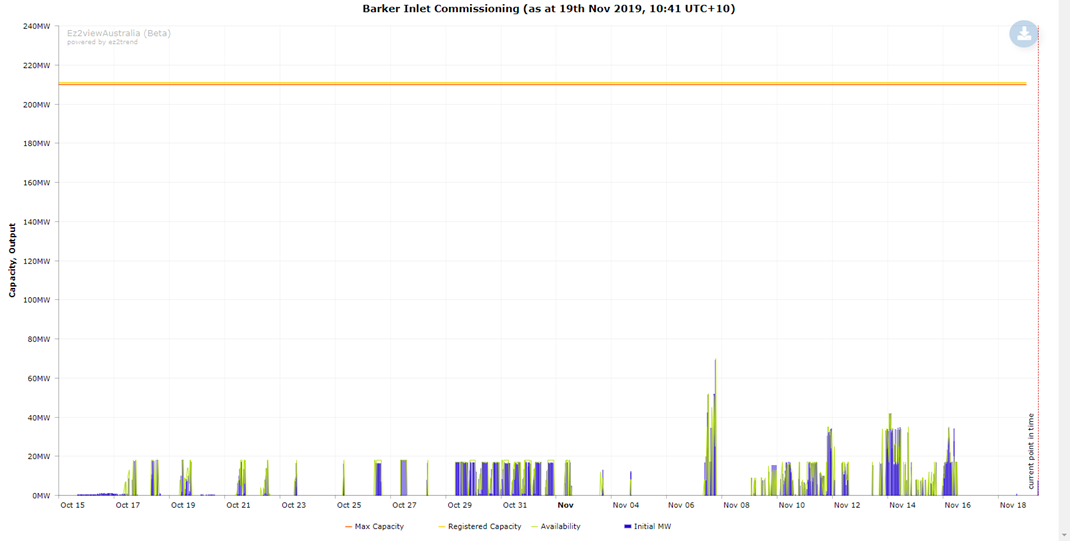

Forming part of the background assumptions in the ESOO were the commissioning of AGL’s new Barker Inlet Power Station (210 MW) on South Australia. Based on AGL’s updates and on the physical generation data we can now see in AEMO’s market systems, for example the following ez2view trend chart, commissioning is underway with at least four of the twelve units having supplied power to the grid in recent weeks:

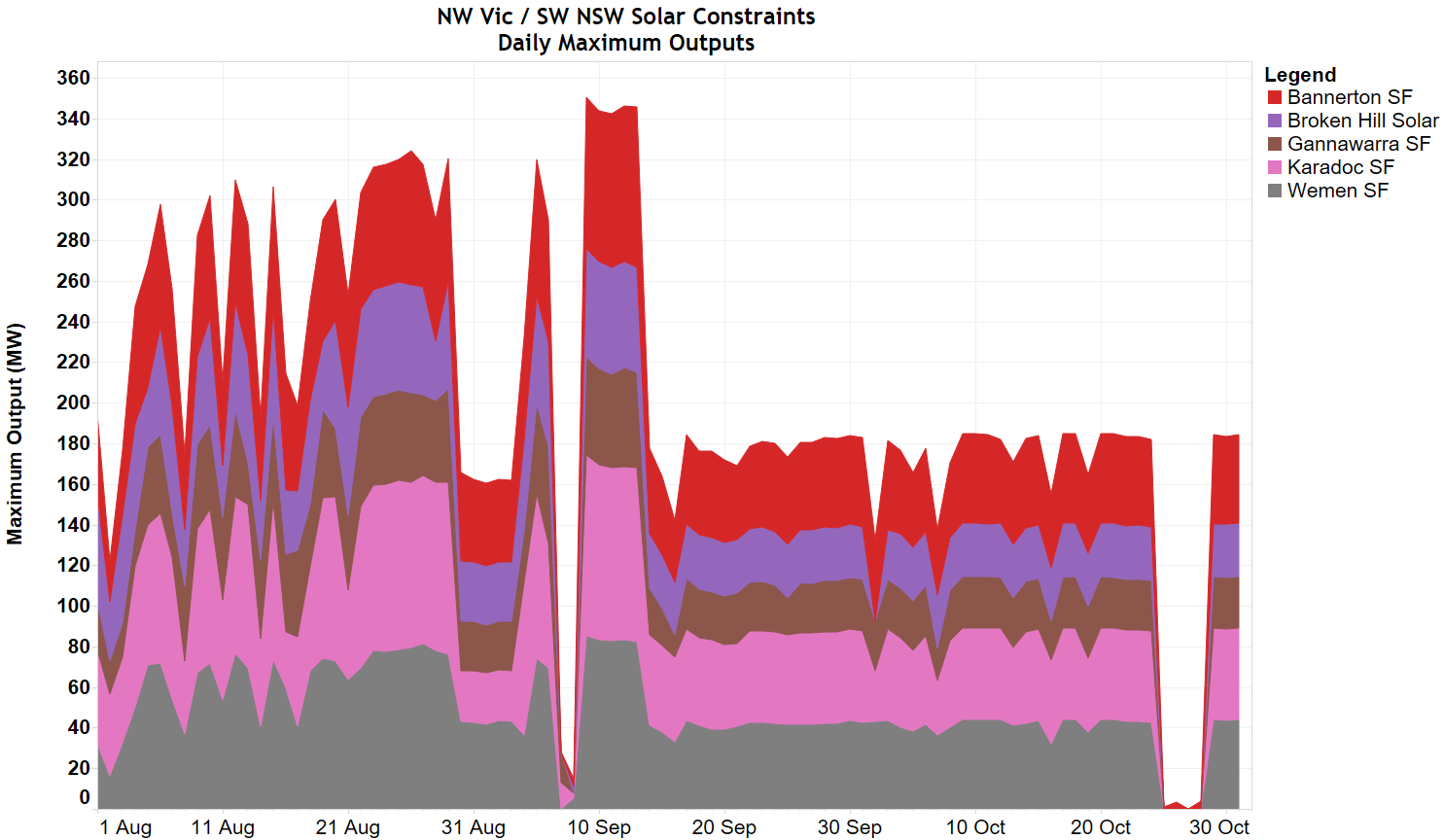

On the less positive side, problems have emerged with voltage stability in the north-western Victorian network where a number of large scale solar projects have connected recently. As a result AEMO has restricted maximum output from five solar farms while it seeks a solution:

The restriction on output amounts to about 160 MW at peak, although the effective contribution of solar generation to supply reliability is a complex topic since it is very dependent on the timing of demand peaks and other supply constraints. It isn’t yet clear when these restrictions will be lifted.

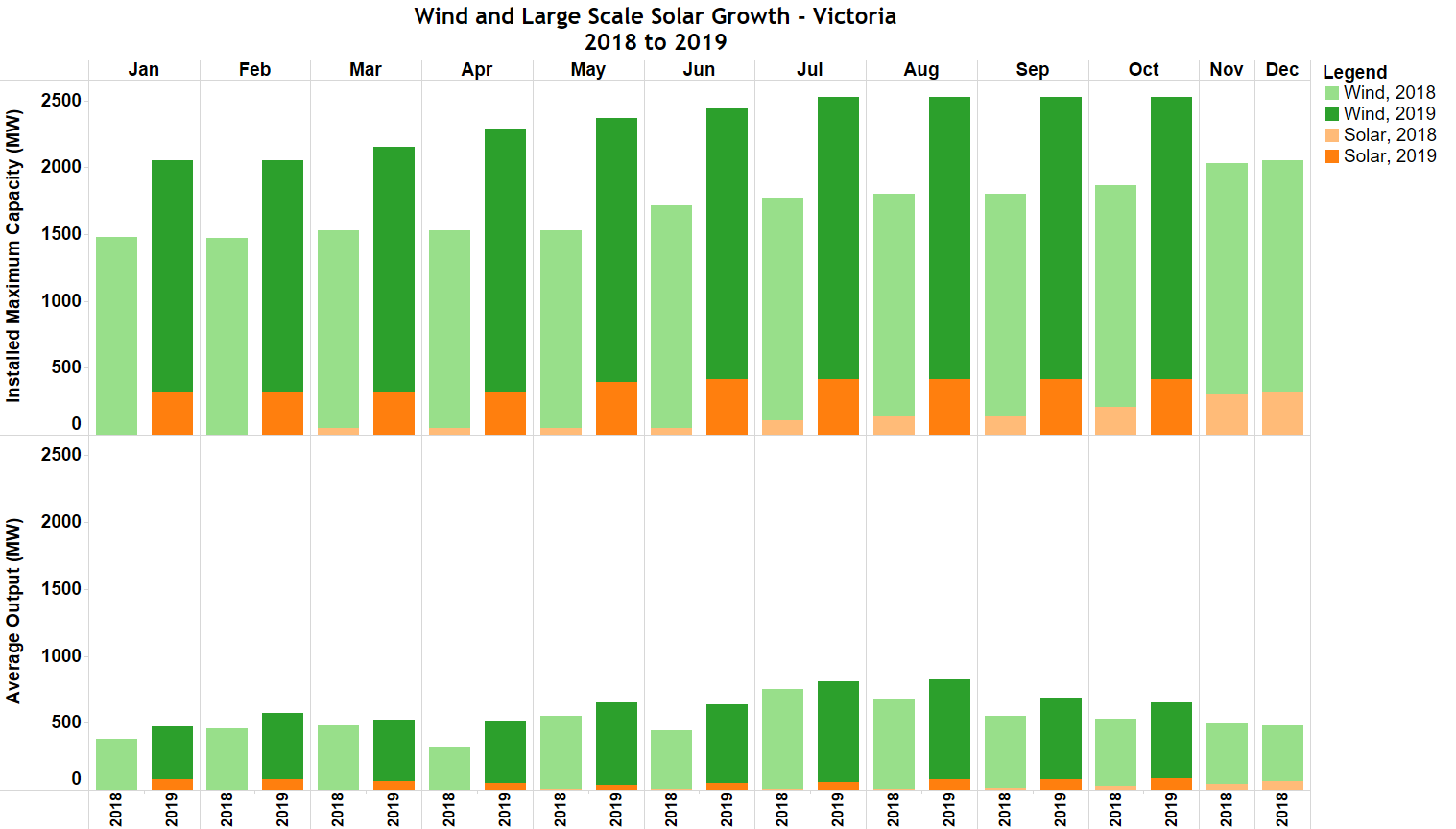

More broadly, we can look at the trajectory of new renewable supply in Victoria over the last two years and how this has tracked over recent months:

The top panel shows nominal installed capacity of large scale wind and solar in Victoria, which has increased by about 500 MW over 2019, although there has been a clear slowdown since July this year. The lower panel shows average output, which is obviously much lower than capacity, given the generation profile of solar and wind production, and dependent on seasonal and climatic conditions. Recent months show that on average, wind and solar (not including rooftop PV, which shows up as reductions in demand seen by AEMO) have added around 100 MW of supply relative to last year although on any given day and time their contribution could be much larger.

AEMO’s MTPASA outlook

The real headline news above is that there are now grounds for a lot more confidence than in the middle of the year – although still not 100% – that the two damaged large generation units will be back in service for the peak summer quarter, which would place the Victorian reliability outlook in lower right quadrant of AEMO’s ESOO table, if nothing else has changed. We note though that this quadrant still assessed potential USE at 0.0013% which satisfies the reliability standard threshold of 0.002% (see my “ConfUSEd by the ESOO?” post for a refresher on what these numbers mean) but is non-zero.

AEMO is probably not going to release an updated ESOO, but its weekly operational MTPASA process produces data on the outlook for supply reliability which we can use to compare the current forecasts for available generation, potential maximum demands, and supply reliability under extreme conditions, to the same outlook at the time of the ESOO’s publication. Here are the two sets of forecasts side-by-side:

I’ve previously posted on how to interpret similar ez2view trend charts of the MTPASA data and won’t go into depth here, but the bottom line is that it’s hard to pick much change at all in the two charts. This might seem surprising in view of the much higher confidence that Loy Yang A2 and Mortlake 2 will be back in service, but unlike the ESOO where AEMO considered discrete scenarios for their return dates, the MTPASA rules require AEMO to use the unit owners’ scheduled dates, which have always been for December returns to service, seen in the step ups in the dark generation capacity line.

The absence of any other significant changes in the generation capacity line, demand forecasts, and supply reliability risks, indicates that any other moving pieces in the reliability puzzle, such as the outlook for renewables contribution or demand levels, have not changed significantly from the time of the ESOO. So, repair gods allowing, we are probably in the ESOO table’s lower-right quadrant world.

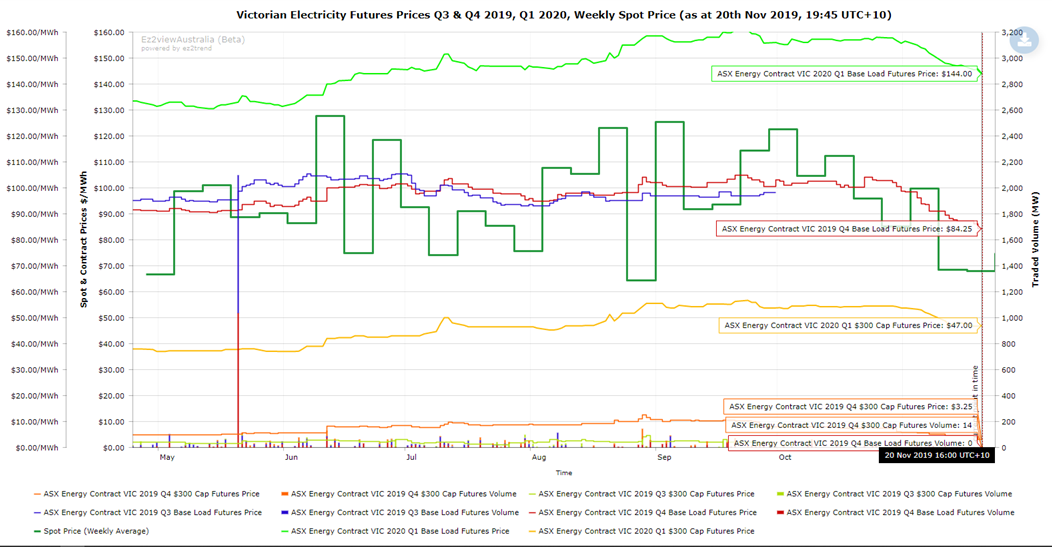

What are market prices telling us?

Like many markets, the traded market in electricity contracts acts as a kind of clearing house for information and risk assessment, as well as for financial transactions. Looking at how market prices have changed recently provides some insight into how the market views the coming summer

The key lines on this chart are contract prices for Vic 2020 Q1 Base Load (bright green) and $300 Caps (orange) which reflect the market’s view on the overall level and potential volatility (above $300/MWh) of Victorian spot prices for January to March next year. These steadily increased through mid-2019, peaking in the month after the ESOO release, but have softened slightly in recent weeks, from about the date of AGL’s update on Loy Yang A2 repairs. We can also see a step down over recent weeks in average spot price levels. Current spot prices don’t imply anything specific about the reliability outlooks for Q1 next year, but are possibly part of the picture feeding into the market’s overall assessments for future price levels.

So why the headlines?

It’s always right to be cautious about the outlook for the NEM, which never ceases finding new ways to surprise us, but most of the objective data I’ve summarised above indicates a better outlook for summer reliability in Victoria than that at the time of the ESOO, particularly the increased confidence on Loy Yang A2 and Mortlake 2. But “better” is only a relative term and the supply-demand balance in Victoria will remain very tight under hot or extreme summer conditions until more dispatchable capacity (including firm demand side response) enters the market.

I do wonder if the effect of some of those headlines – or rather the politics behind them – is actually scaring away potential providers of that capacity, who may see nothing but increased risk of further unexpected and often unhelpful political interventions.

——————————————-

About our Guest Author

|

Allan O’Neil has worked in Australia’s wholesale energy markets since their creation in the mid-1990’s, in trading, risk management, forecasting and analytical roles with major NEM electricity and gas retail and generation companies.

He is now an independent energy markets consultant, working with clients on projects across a spectrum of wholesale, retail, electricity and gas issues. You can view Allan’s LinkedIn profile here. Allan will be sporadically reviewing market events here on WattClarity Allan has also begun providing an on-site educational service covering how spot prices are set in the NEM, and other important aspects of the physical electricity market – further details here. |

Thankyou for a very good analysis but if we take Jan 25th as a the base case where we were short 200 MW and coal was only supplying 3,400 MW instead of a rated 4,700 MW, we have already experienced a situation with 4 of 10 generators being off on a hot day.

One can say that if we had had 300 MW more supply/ less demand we would have been OK. We will have almost 400 MW of behind the meter solar, 600 MW of utility solar and about 900 MW of wind additional capacity. Usually hot days are more like today where minimum wind generation in Victoria between 10 am and 7 pm was about 850 MW whereas 25 Jan was very unusual in that wind varied between 380 and 810 MW

Due to difficulties connecting wind and solar farms the installed capacity growth has been much faster than energy delivered, some wind plants are also being constrained down as well as the solar.

I think it is hard to see that demand will not be reduced by at least 200 MW from 9 till 3 due to rooftop supply and new utility wind and solar will provide a minimum of 1,000 MW and an average of 1,500 MW, vs 450 MW min and 800 MW av on January 25th. Today for example wind in Victoria only averaged a bit over 45% CF so it wasn’t a particularly good wind day and yet wind generation was more than double that of January 25. Further at 1 PM on January 25 imports from NSW were zero. NSW will be generating at least 400 MW of new wind and solar in the west and the Riverina, surely some of that will find its way south to Victoria even if it is only 100 MW.

But it is also a reasonable bet that if there is really a small reserve margin, that ways will be found for at least a temporary increase in allowable power from these constrained northern and western Victorian assets, so I suspect if coal drops by another 500 MW at least 250 MW of wind and solar would be found, adding to the 850 MW swing in the demand supply balance mentioned above.

Farley, VIC wind contributes about 10% of nameplate capacity to peak demand. Solar contributes zero.

You don’t have to exaggerate here like you do on the other blog, it’s not necessary, just the facts are fine. Everybody know that no matter how much nameplate capacity of wind is installed, it may not be there when it’s needed.

Having spent years commissioning power stations and other large rotating equipment, I suggest the risk of the two replacement generators having teething issues is understated.

Additionally there will be performance testing and bedding in periods required by the OEMs. “Online” is a good milestone, but doesn’t necessarily mean “fully available”.

It seems to me that last summer was the harbinger of things to come. Tight supply is the new normal, regardless of how much wind and solar go in.

Thanks for the comments Peter & Ben – they both identify important issues and illustrate the complexities of the reliability puzzle, particularly as your conclusions tend in opposite directions. I’ve tried to put some thought into a response.

First some context on Jan 24 and Jan 25 last summer. On both days there was forced load shedding (smelter on day 1 and Victorian consumers on day 2), as well as AEMO calling on load reductions from its portfolio of contracted RERT customers.

Demand and supply conditions were different on the two days. Jan 24 saw a combined SA/Vic shortfall with extreme SA temperatures (~46 degrees) and very hot weather in Victoria (~41 degrees in Melbourne). Two large Victorian coal units were out. The supply shortfall emerged in the late afternoon / early evening as rooftop PV production fell away, increasing grid demand, and wind production across both states reduced to about 15% of installed capacity. Smelter load cut and RERT calls in Vic reached about 400 MW of demand reduction.

Jan 25 saw a Victoria-only event, with temperatures of 43-46 in the Melbourne area following the previous day’s high temperatures – consecutive days of heat also elicit significantly higher demands than the first day of a heatwave. Cooler weather in SA enabled exports to Victoria up to interconnector secure limits, but offsetting this a third coal unit had failed. RERT load reductions of up to 450 MW were called by AEMO but as demand continued to climb and wind production reduced to around 400 MW (roughly 20-25% of Vic wind capacity), rolling area blackouts commenced from midday local time – these reduced demand by around 200-300 MW. Significantly longer and deeper load reductions would have been necessary had rising underlying demand not been arrested by an early afternoon cool change accompanied by increased winds and higher windfarm output. Victorian rooftop PV and large scale solar output was over 1000 MW during most of the load shedding period.

Both days were good illustrations of low probability but high consequence events that can contribute disproportionately to reliability risks. Very hot weather is not always coincident across SA and Victoria. Based on historical outage data for the ten Victorian coal units, the chances of three units being out on the hottest day of summer, Jan 25, was of the order of 1.6%. (Even with doubled forced outage rates that risk would still be only around 8.5%). Combined with that day being one of extreme temperatures – well above those expected on the hottest day of a “median” summer, this may all look like a very improbable outcome.

But there were also a multitude of favourable factors that don’t get as much notice as the negatives – there were no significant gas, hydro or transmission outages, renewables output was broadly speaking in line with or even above median levels for the time of year, the cool change arrived before the afternoon / evening demand peak on Jan 25 and so on. And even if only two coal units had been out on Jan 25 there still almost certainly would have been shedding, perhaps even the case with only one unit out.

Because of all these moving and uncertain parts it’s basically impossible to draw clear conclusions about reliability by using “single point” estimates – even quite conservative ones – of what levels demand, thermal output, renewables etc etc might reach, or how many units might be off, to conclude that there will or will not be supply shortfalls this summer. I don’t see much alternative to the type of probabilistic modelling that AEMO runs for the ESOO which can test literally hundreds or thousands of combinations of the myriad factors with associated probability distributions.

The result of AEMO’s modelling for this summer is that – assuming LYA2 and Mortlake 2 are back in service – they estimate that the “risk x consequence” of supply shortfalls (USE measure) is a little lower this summer at 0.0013% than it was leading into last summer at 0.002%. Behind that number are many scenarios – probably a majority – where there are no shortfalls (Peter’s point) but still a significant proportion where there are (Ben’s point). In a sense you could both be right.

It is interesting that the two interpretations of the same event both contain elements of truth. Part of the deal with Aluminium smelters, paper mills etc is that if you get power at 1.4-2.5 c/kWh, you are expected to drop demand in emergencies. It is common practice throughout the world including in Germany where customer downtime is an average of 12 minutes vs our 2.5 hours per year.

As you say wind output on the day was a bit higher than the previous 10 days but only half that of December the 9th, the first hot day of this summer. The cool change was definitely a help but another coal generator Loy Yang A 2 went offline at about 5 pm, more or less offsetting the reduction of demand.

I am not sure how you can claim that there would still have been load shedding if there were only two coal units out, because Yallourn 3 and 4 which were both offline by 1 am were 375 MW each and Loy Yang A1 of 500 MW was offline. Loy Yang A2 never got above 75% capacity and finally gave up at about 5 pm so during the critical period from 10:30 till 6 PM, coal generation was down by 1550 to 1850 MW. One Loy Yang unit and one Yallourn unit is a total of 880 MW. Even if we had one of each out and Loy Yang A2 struggled along at 75% capacity we still should have had 3,500 MW of coal which would have been enough to avoid blackouts

However on the overall point it is ridiculous to demand that we eliminate all risk of USE in a spindly grid like Australia’s where 95% of outages are T&D related. Back in 2009 we had three load shedding events of about 1,000 MW. Did the world stop.

Increasing use of local resources can in fact reduce the likelihood of cascading widespread blackouts. For example in Adelaide during their storm blackout, when the storm warning was issued if they had increased gas generation by a mere 150-200 MW, thereby increasing the headroom on the interconnector, no more than rotational shedding for half an hour to an hour would have been required. If South Australia’s current battery capacity had been available at the time probably no urban or Southern blackouts would have occurred at all

The most charitable thing to say about Ben’s comments is that he hasn’t looked at renewables output graphs for the last few years

Peter my comment that load shedding would still have been likely on 25 January with only two units out is supported by AEMO’s 2019-20 Summer Readiness report which quantifies general customer load shed that day as up to 538 MW (on top of RERT reductions of 625 MW). An extra Yallourn unit wouldn’t have covered this gap, while an additional Loy Yang unit would have left the balance very marginal.

And I don’t disagree that in the majority of circumstances the additional wind and solar commissioned in Victoria should leave supply-demand balance better placed than last year.

Allan