Linton is a Senior Software Engineer and Market Analyst, who joined Global-Roam in August 2020.

Before joining the company, Linton worked at the Australian Energy Market Operator (AEMO) for seven years, including four years as an analyst within their demand forecasting team. Before entering the energy sector, he worked as an air quality scientist in the Czech Republic.

Taking a quick look – after our ez2view ‘Notification’ widget triggered an alert for what appears to be Callide C4 tripping from close to full load (Sunday 9th November 2025 at 21:26 NEM time)

The first day of scorching summer temperatures for the year has been matched with elevated electricity prices in New South Wales, Victoria and South Australia for most of the day. Queensland and Tasmania experienced small patches of high prices yet…

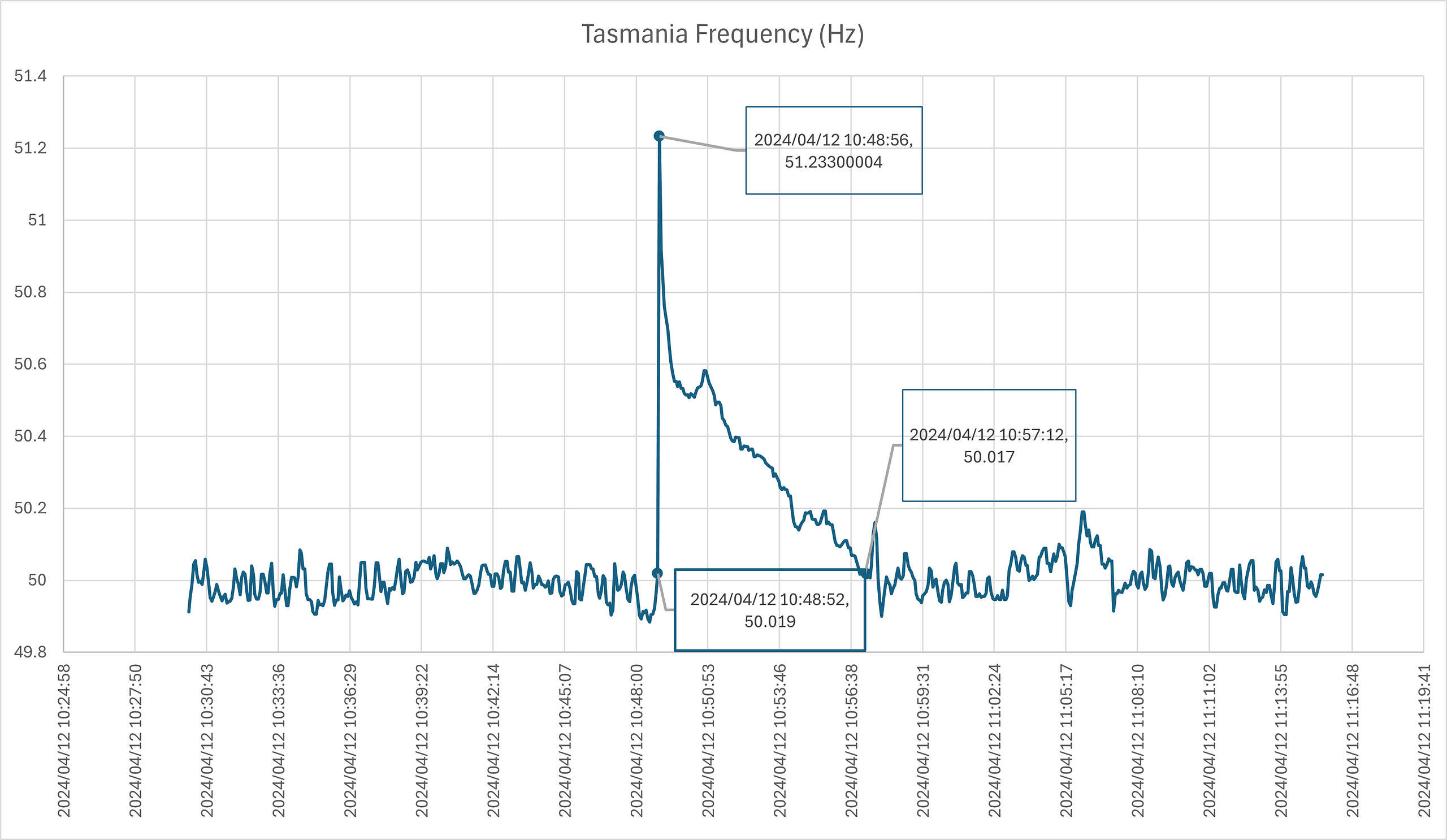

Be the first to commenton "Tasmania’s grid frequency on Friday 12 April 2024"

Be the first to comment on "Tasmania’s grid frequency on Friday 12 April 2024"