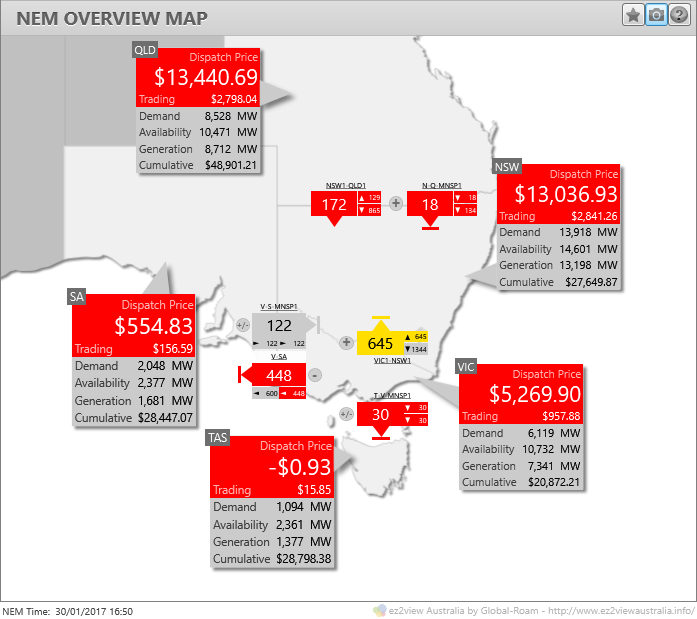

At 4:45pm AEST yesterday, the start of dispatch interval (DI) 16:50, spot prices suddenly spiked in the three largest NEM states, viewed here on ez2view’s NEM Overview Map widget:

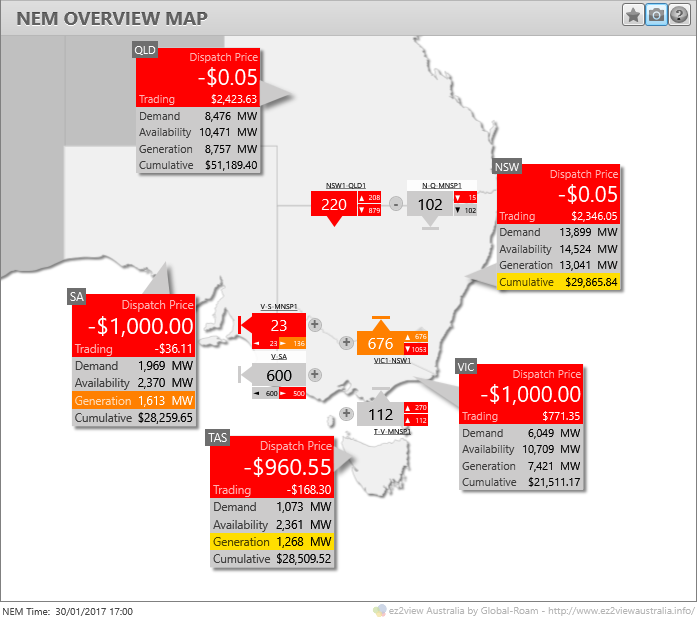

Those high prices lasted for just that single DI, and 10 minutes later we saw this picture:

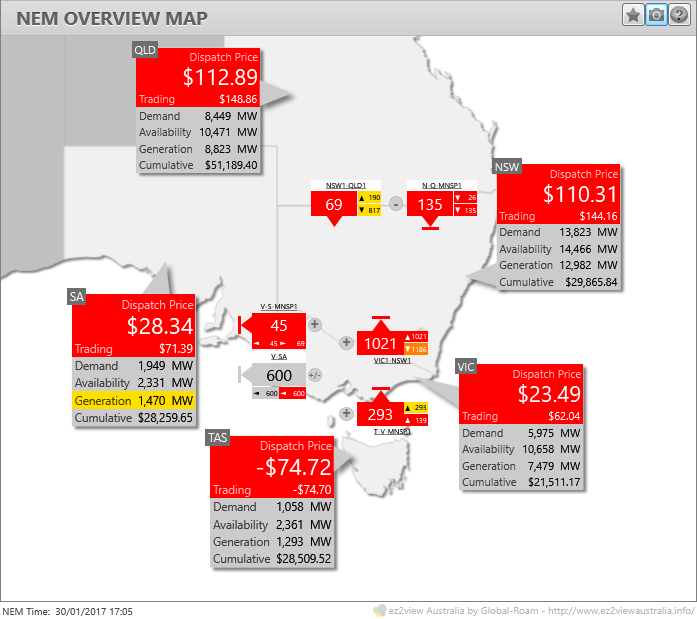

By the next DI, things were back close to normal, which is more or less where they stayed for the rest of the evening:

So what was that all about?

Unfortunately a full answer would be complicated and time consuming – both to investigate and then to explain. The NEM can be a very complex animal. In this review I’ll just try to touch on some key factors, which in summary seem to be the following:

- Brutally hot weather in NSW – approaching 44 degrees in western Sydney – driving demand to very high levels. Queensland demand was also strong.

- Transmission constraints limiting the ability of Victorian generation to flow northwards into NSW to help meet those high demands. In particular the NEM’s own unique version of the rail gauge problem reared its head.

- Bidding behaviour also contributed

NSW Demand

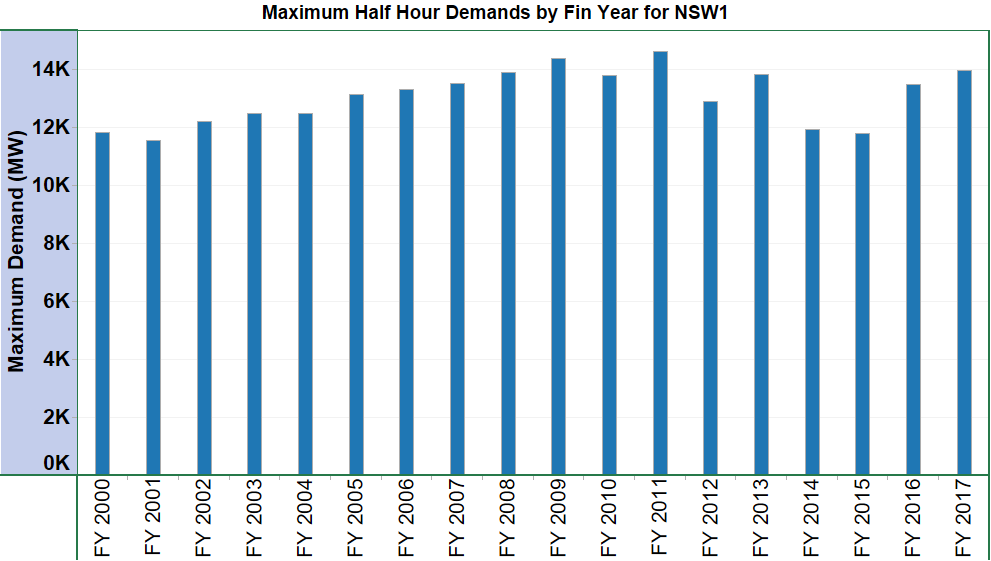

5 minute scheduled demands in NSW exceeded 14,000 MW around the late afternoon / evening peak and even half hourly averages – AEMO’s customary Maximum Demand metric – approached that level, which hasn’t been seen since the summer of 2010/11

Fortunately all the major thermal power stations in NSW were available and running at near full capacity, but even with about 14,600 MW total of local generating capacity available, interconnector imports – especially from Victoria where demands were subdued leaving plenty of spare generation capacity – were important in generally keeping a lid on spot prices through the day.

Transmission Constraints

Constraints on power flows within and between NEM regions, to maintain secure operation of the network, are a crucial feature of the NEM.

Interconnector constraints which limit flows between NEM regions are a well known example, and most readers will be familiar with seeing price separation between regions when no additional power can securely flow from a lower-priced region to a neighbouring high-price region.

Less well known is that many if not most of these “interconnector constraints” aren’t actually anything to do with the transmission lines that physically cross NEM regional boundaries, but with equipment and conditions elsewhere in the network. And that’s where the rail gauge analogy comes in, because one of the key constraints operating yesterday originates from the fact that back when the Victorian and NSW power systems were run by separate state-owned entities (dare I say “fiefdoms”?), they decided to standardise their highest capacity transmission lines at that time on different voltage levels – 500 kilovolts (kV) in Victoria and 330 kV in NSW.

The end result was that the key lines between NSW and Victoria, built in the days of the Snowy Scheme’s construction, still operate at 330 kV but within Victoria most large generation is nowadays connected to 500 kV lines (and the rest at 220 kV). So moving power from Victoria to NSW requires 500kV/330kV transformers, actually located at South Morang near Melbourne, and these can be a crucial bottleneck on northward flows.

On the first couple of screenshots above, the flows from Victoria to NSW are constrained at around 650-700 MW, and were limited by this South Morang transformer capacity constraint. The 330kV transmission lines linking Victoria and NSW can themselves carry considerably more power than this.

All this meant that AEMO’s dispatch process was limited in its ability to use “low cost” generation in the southern part of the NEM to supply demand in NSW or Queensland.

Bidding Behaviour

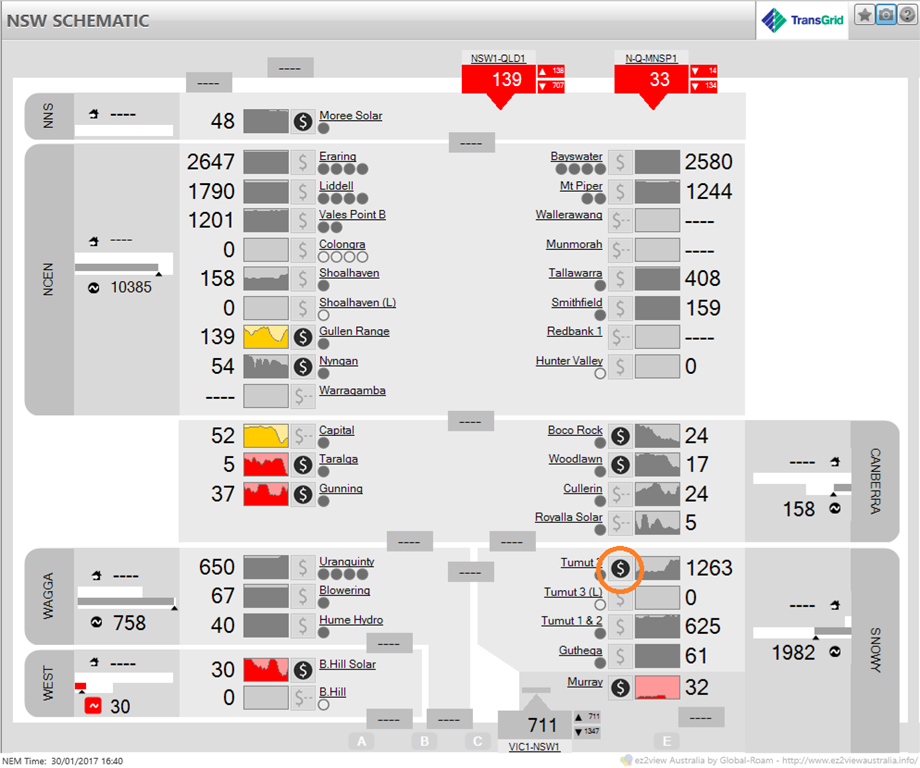

Generator rebids, together with some tightening on the Vic-NSW interconnector limit (which moves around dynamically as network conditions change), may have been the final trigger for the event at DI 16:50, since there were no major changes to demand, generation trips etc in the northern regions. Looking, the day after the event, at ez2view’s Region Schematic widget for NSW , we see evidence of a couple of rebids that moved low-priced capacity to high-price bands just before the spike. In DI 16:40

The important rebid here is from Tumut 3, indicated by the circled ‘$’ symbol. A summary of this rebid appears in ez2view when hovering over the symbol:

The last two lines show that 100 MW of capacity has been repriced from $299.80/MWh (which happens to be the NSW dispatch price for this DI) to $13,999/MWh.

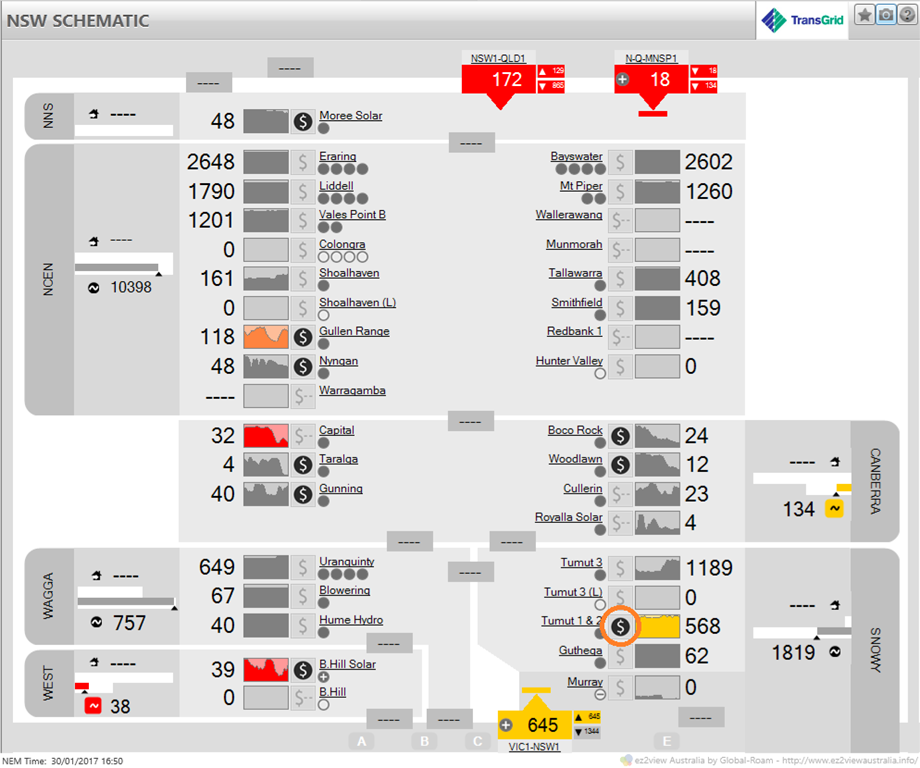

Then in DI 16:50 itself, a rebid at Upper Tumut, moving a bit more capacity (80MW) to high price bands:

With the constrained flows from the south dropping a little, these rebids and the limited spare, lower priced capacity available in Queensland and NSW being fully utilised then left the spot price in the northern regions with nowhere to go but five-digit territory.

As for reasons why the price in Victoria also leapt to over $5,000/MWh at the same time, and the SA price jumped, less dramatically, to over $500/MWh – well, these are very complex but have to do with the detailed operation of the very same transmission constraint limiting flows into NSW from the south. I’m unable to go into the details here, but very roughly, high prices in NSW/Qld can “echo back” into other NEM regions due to the mathematics underlying the way this constraint and others operate, and the way dispatch price is determined.

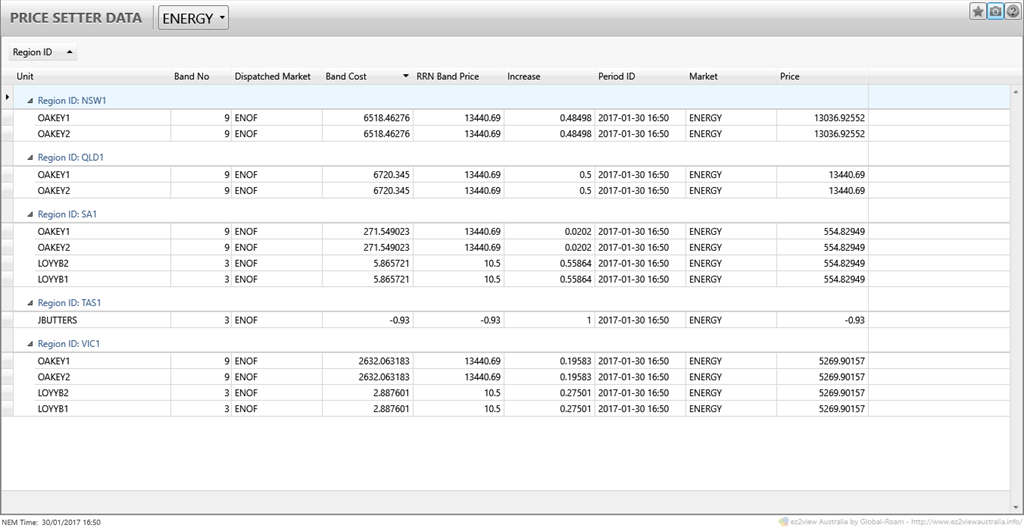

ez2view’s Price Setter Data widget shows which bids at which NEM unit or units are effectively setting each regional price and for the 16:50 DI it shows very high price bids at Oakey power station in Queensland are not only setting price in NSW and Queensland (effectively one region under yesterday’s conditions) but also contributing to prices in all mainland NEM regions:

Finally and very briefly, the cause of those subsequent –$1,000/MWh prices comes down to the same reason cited in an earlier review – after a price spike, generators can be strongly incentivised to rebid more capacity at low prices in an attempt to increase their output, because of the “5/30” settlement price effect. They did this in spades after the 16:50 price spike yesterday resulting in that brief drop in dispatch price to the market floor in the south of the NEM, and close to zero in NSW and Queensland.

|

Allan O’Neil has worked in Australia’s wholesale energy markets since their creation in the mid-1990’s, in trading, risk management, forecasting and analytical roles with major NEM electricity and gas retail and generation companies.

He is now an independent energy markets consultant, working with clients on projects across a spectrum of wholesale, retail, electricity and gas issues. You can view Allan’s LinkedIn profile here. Allan will be regularly reviewing market events here on WattClarity. Allan has also begun providing an on-site educational service covering how spot prices are set in the NEM, and other important aspects of the physical electricity market – further details here. |

Leave a comment