The emergence of new entrant energy retailers represent a significant threat to the ‘big three’. There are a number of reasons for this and the story is set to play out further in 2015.

(1) New retailers approved

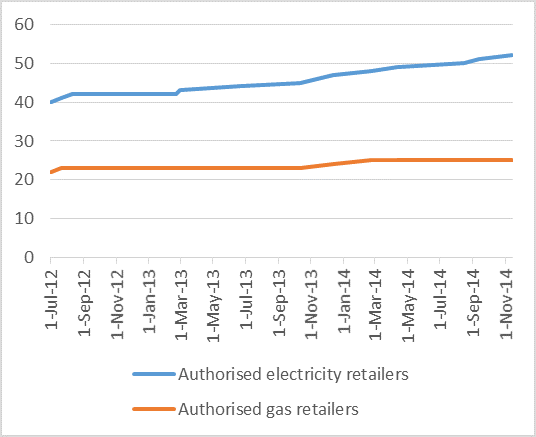

Attracted by the prospect of taking market share and retail margin, a large number of new entrant retailers have applied for and been granted retail authorisations from the Australian Energy Regulator. In the last 18 months, the Australian Energy Regulator has granted nine electricity retail authorisations, together with more than 35 individual exemptions from the requirement to hold an electricity retail authorisation (typically companies offering solar PPAs).

Combined number of current gas and electricity authorisations issued by the Australian Energy Regulator

Source: www.aer.gov.au/node/1265 as of 15/11/2014

(2) National Regulations making it easier to join the party

The gradual implementation of the National Energy Consumer Framework (NECF) (currently applicable in NSW, SA, TAS and ACT) has had the effect of emboldening new entrant electricity retailers. The NECF means that a company can apply to the AER to retail electricity in all NECF jurisdictions, whereas they would previously have to apply in each separately.

The harmonisation of energy retail regulations as a result of the implementation of the NECF has most certainly made it easier for electricity retailers to comply with their obligations and for new companies to enter the market (refer to www.aemc.gov.au/Energy-Rules/Retail-energy-rules/Guide-to-application-of-the-NECF for a summary of the NECF).

Electricity retail is a highly regulated industry (perhaps to the benefit of not only consumers but also lawyers…). The rules cover the operational, technical and financial aspects of energy retail (in other words, basically everything) and are there to ensure integrity and reliability of the market as well as for the protection of consumers.

(3) Less actual or perceived volatility in the market

The three main barriers to entry for new entrant retailers are:

1) lack of understanding of the wholesale market and the risk management tools required;

2) lack of capital to support the operational, wholesale and prudential requirements; and

3) concern about the volatility of the price of electricity on the wholesale market.

On the first point, there are plenty of great tools such as NEM-Watch to assist in understanding the market. On the second point, there are also a few investors who are okay with a lack of return for a few years whilst a retailer is established. On the third point, new entrant retailers have been watching the market and can see that there has been less volatility in pricing since 2009-2010. They also appreciate that this trend is likely to continue, as we have excess generation and falling demand thanks to demand side efficiency and solar (and soon with battery storage).

With new and proposed regulations further restricting the operation of generators and others, new entrant retailers also appreciate that there is less opportunity for them to be ‘gamed’ by the other players in the market.

(4) Consolidation in the Middle

Whilst the bottom end of the market is getting crowded, there is space in the middle. As noted in a previous WattClarity article, ‘Incumbent Retailers under siege on both sides’:

“Since the NEM started many years ago, we’ve seen the initial group of retailers grow smaller and smaller over time – as Origin, AGL and EnergyAustralia have gobbled up pretty much everyone else who was there at the start.”

New entrant retailers see this gap in the market and most are looking to eventually get into that space. New entrant retailers also sense that many incumbents operate with inefficiencies, struggle with legacy billing systems, and generally think they can do a better job.

Lastly, new entrant retailers know that there will be more acquisitions and there will be further consolidation. For many new entrant retailers, particularly those with a small base of investors, the exit strategy is a sale within the next five years.

(5) Consumer malaise presents opportunity

Consumer dissatisfaction with current providers provides leverage to new entrant retailers, who are keenly aware that people don’t have a great degree of loyalty towards their existing energy retailers. After all, it is hard to develop a brand around a product that no one can touch or see. The only experience people have with their electricity retailer is when they receive their bills, or when the lights go out (and when they do, they blame the retailer not the network company).

Customer dissatisfaction with electricity retailers has risen dramatically over the past five years. This is partly a result of affordability issues, as the price paid by consumers has risen dramatically and people have been struggling to pay their bills. Customers don’t necessarily see a distinction between network components and the retail margin represented in their bill.

Last financial year, the Energy and Water Ombudsman NSW (EWON) received 30,349 electricity related complaints (see page 18: EWON Annual Report 2012-2013). Although compared with the previous year this increase was noted as ‘modest’, in comparison to the number of electricity complaints to EWON in 2010-2011, it represented an increase of 153 per cent (see page 14: EWON Annual Report 2010-2011). Similar figures were seen in other States. In Victoria in 2012-13, there were 56,795 electricity cases reviewed by the Energy and Water Ombudsman (Victoria) (EWOV), representing an increase of 19 per cent from the previous year (see page 3: EWOV Annual Report 2012-2013).

Seventy eight per cent of complaints received by EWON in 2012-2013 were lodged against the big three retailers Origin Energy, EnergyAustralia and AGL. Whilst those three supplied approximately 77 per cent of small electricity customers (see page 120: AER, State of the Energy Market 2013), the overall conclusion is that there are plenty of unhappy energy consumers—and their unhappiness is increasing.

For a new retailer, this represents opportunity. It is much easier to keep 5000 customers happy than it is to satisfy 5,000,000 customers. Smaller retailers operating in niche markets are able to focus on higher margin customers and ensure that those customers are not lost in a legacy billing system.

(6) Power to the People

Consumers are responding positively to new entrant retailers. In 2012-2013, the combined market share of the top three fell by 2 per cent (see page 120: AER, State of the Energy Market 2013).

Ultimately, the beneficiaries of increased choice will be energy consumers, not only in terms of pricing but also by improved customer service, better delivery of service, new products and blended offers combining grid energy with products such as solar.

Watt-ch this Space

With the larger number of retailers now operating, there is obviously a greater risk that one will fail or that consolidation of the market will be required (assuming that retail margins may not be as profitable as they currently are or are perceived to be). The financial capacity of electricity retailers will undoubtedly be a focus of energy retail regulators such as the AER, ESC and AEMO.

One thing is certain; 2015 is shaping up to be an interesting year in the retail market. New entrant retailers are beginning to offer hybrid products combining grid energy with solar, lighting, energy management and, of course, storage. We are also likely to see stronger responses from incumbents to this increasing threat to their business model.

About our Guest Author

|

|

Connor James is a qualified solicitor with extensive experience in the regulations applicable to energy retail. Connor specialises in helping new entrants obtain electricity retail licences and develop compliance programs.

Connor is the director and founder of Permitz Group which is focused on different areas of licencing.

Permitz Group has worked for many leading companies including Sony, Toyota, Suzuki, Hilton Hotels and JB Hi-Fi. Connect with Connor via LinkedIn here. . |

Leave a comment