This article by David Leitch & Ben Willacy was originally posted on RenewEconomy, where there are other comments. Reproduced here with permission.

The NSW Liberal government’s announcement for its renewable energy growth plans seals the death warrant for about 6 gigawatts of coal capacity, and is very bad news for the owners of the same.

By 2030, we expect around 6GW of currently operating coal generation will be surplus to requirements. Exactly which generators will close and how soon will depend on competition. In ITK’s main model we have, in previous runs, constrained NSW coal generation to a minimum of 2GW up to 2030. That seemed academic a couple of years ago, but is a live issue now.

In short, if we continue to constrain NSW to have minimum coal generation then all the brown coal generators in Victoria will be in deep trouble. On our numbers all three would be faced with unachievable ramp issues by 2030, which perhaps a battery could help with in theory, but capex likely not justifiable. In that scenario we think it very likely Yallourn will close around 2025.

If, alternatively, we dispatch entirely on merit order, that is lowest variable cost to highest, then it’s the higher cost black coal generators in NSW that bear the pain. In practice, the reality is that neither AGL or Origin will allow Bayswater or Eraring to run down towards zero every day. They will most likely see that by taking short-term losses they can force Yallourn out of the market.

Caveat: Its also important to note that we have not considered inertia, frequency, voltage and system stability in this analysis. To the extent that AEMO, and the AEMC still don’t have processes in place to ensure those system services can be provided by 21st century technology (read batteries and virtual synchronous machines) then it may be that AEMO will constrain wind and solar off if leaving it on makes coal generation likely to close. We know the answers to this problem but the NSW announcement ups the ante again for rulemakers. State Governments wouldn’t be doing all this stuff if the Federal Government had made policy and if the AEMC had been more forward looking. Nature abhors a vacuum.

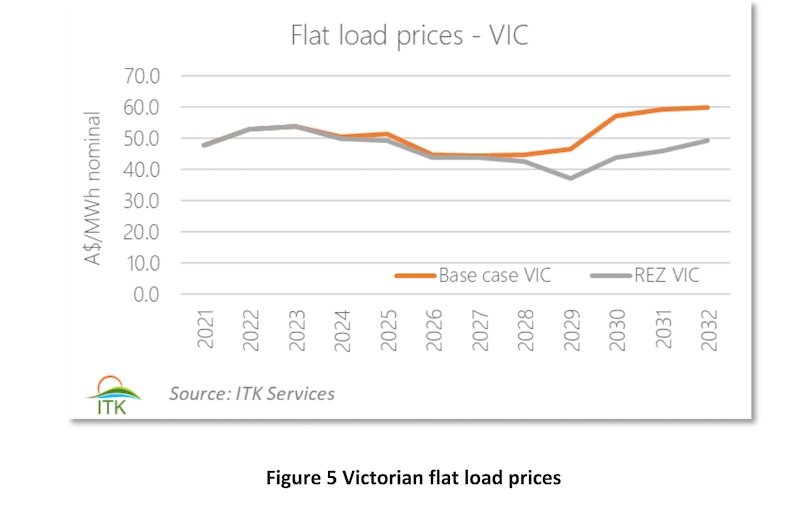

Flat load prices $15/MWH lower by 2030 compared to prior estimates

We expect prices to fall around $15/MWh compared to our prior forecast as a result of the NSW announcement although mostly towards the end of the decade. We do expect volatility around the coal generation closures and offer a ray of hope in that the low prices may be enough to keep things like aluminium smelters running.

Thumbs down to AGL, CLP and ORG as investments

Nevertheless what we are left with is the losers. They are CLP (The owners of Energy Australia and Yallourn), AGL, ORG and Alinta and probably some assets owned by Stanwell and CS Energy in QLD that we haven’t got round to yet. Profits for these companies unless they dramatically change strategies are likely to be worse than expected on average.

I have to focus on AGL and ORG because they are listed in Australia but one could include CLP. The management of these businesses have behaved like incumbents in any industry. They don’t believe what’s happening, underestimate the change and try to influence Government to slow things down. AGL, as we have written before, is by far the most culpable because it deliberately bet against climate change and renewable energy when it bought Macgen (the NSW coal assets) and increased its interest in LYA (Loy Yang A in Victoria). That was company-destroying misjudgment.

Even today, management of all three big gentailers seems to see wind, solar, and behind-the-meter as nothing but a threat. None of them has anything of interest to tell investors and investors have largely washed their hands of them. AGL has signed a couple of battery PPAs and maybe one solar PPA in the past few years.

ORG and CLP have essentially done nothing more than the minimum to meet their mass market LRET requirements and nothing new in recent years. Further, the management of all three appears to have given up. Finding a way forward isn’t easy but Orsted and Nextera have shown what’s possible, Orsted being a more recent example. This note focuses on generation, but the majors are also losing share in retail, about 1/7th of the mass market volume is behind the meter, and corporate PPAs have taken say 2.5% of the larger than mass market volume.

What the NSW goverment announced

The NSW government announcement is still short on numerous details, but the key elements as far as ITK is concerned are:

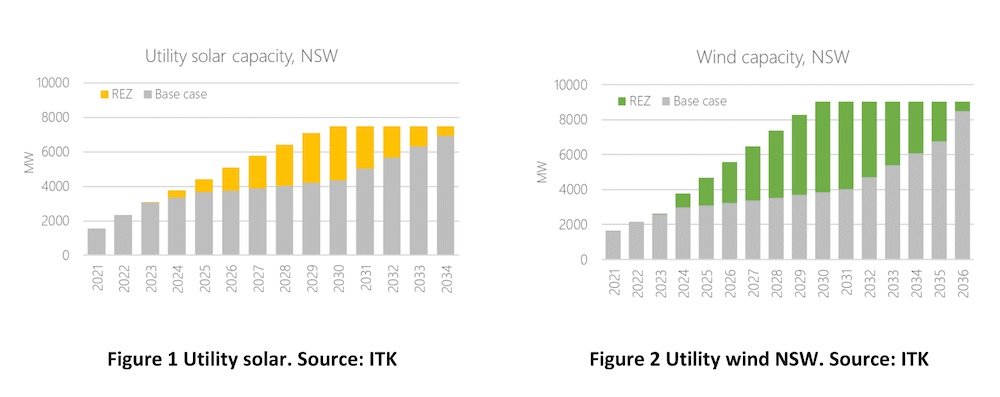

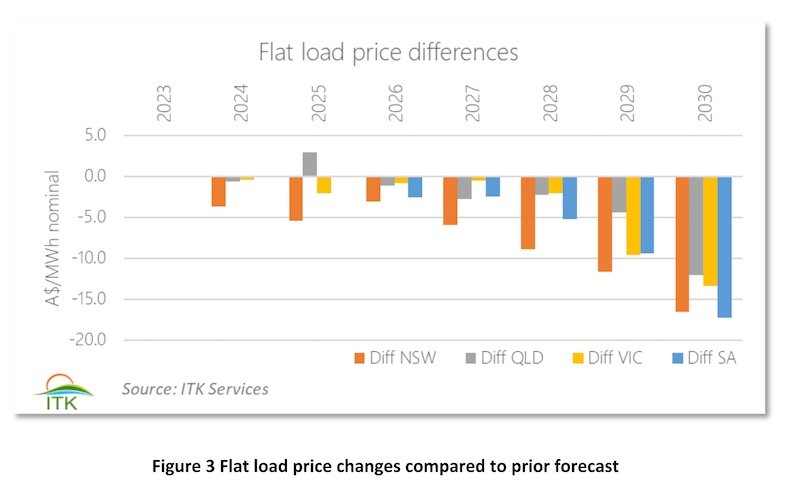

- Financial support for 12GW of wind and solar to be built between 2022 and 2030. We expect the timetable will slip a bit but do not model it to in the first instance.

- A reverse auction for swaption contracts – the government provides certainty around minimum revenue using a swap/CfD, and generators hold the option to exercise these contracts

- Potentially signing contracts with retailers to provide the retailers with access to the NSW underwritten wind and solar.

- The steady development is expected to result in efficient development, ie avoid boom bust, take advantage of learning rate. One crew moves from one project to the next. All very good stuff.

- Any net cost of the support will be recovered from distributors who will pass it on to customers. (question whether distribution pricing is equitable in that solar households pay less network costs than others)

- Financial support for 2 GW of storage with >8 hours duration, with preference for >12 hours, again to be built by 2030.

- A unique to NSW Transmission Efficiency Test [TET]. The test would involve making a declaration that a proposed transmission line is a ‘declared REZ transmission line.’ The Independent Regulator would then be required to conduct a comprehensive assessment to inform a determination of the prudent and reasonable costs that can be recovered. The transmission company would then be required to develop the project and would be entitled to the level of cost recovery and would recover that from generators.

- Various NSW Govt bodies to manage the process.

ITK’s takeaway analysis headlines

There is too much in this announcement to deal with in one piece of analysis. In this note we focus on the 12GW of wind and solar. In particular, we look at:

- Its impact on electricity prices compared to ITK’s prior estimates;

- The impact on thermal fuel market share.

There are a bunch of other things of interest, such as spilled solar and or wind, the change in the use of transmission and indeed whether the announcement changes transmission investment quantity or timing. However, that analysis will have to mostly wait till later.

Before getting into the numbers, it’s also worth pointing out that, even though ITK has long been more aggressive than most other serious modelers in our base case assumptions about renewable penetration, we still didn’t and don’t have Queensland getting to 50% by 2030, “only” 38%. So there is still more to come.

Our approach

To analyse the impact of the NSW government announcement, we have used our NEM forecasting model and adjusted the inputs to reflect the wind and solar growth flagged by the roadmap. We already assumed massive growth in VRE (variable renewable energy) generation in New South Wales, and that growth will need to continue beyond the volumes prompted by this policy. We therefore see the roadmap as an acceleration of medium-term growth.

We do not know the schedule that the new Consumer Trustee will use to bring new generation online, but we assume it will be done sooner rather than later. It could take a conservative approach, carefully matching supply with forecast requirements. But this is hard to do in practice, and we expect the Government will focus on getting generation in place well before it is needed.

We have therefore assumed a gradual growth in capacity in the Central West Orana renewable energy zone (REZ), between 2023 and 2030, and the New England REZ between 2024 and 2031. We note that the timeframes for building the REZ infrastructure are a key risk to this outlook.

For the purposes of this note, we refer to our prior modelling inputs and results as our “base case”, and to the impact of the NSW Government’s Electricity Roadmap as our “REZ” case.

We have made no changes to our storage volume assumptions. We already allow for large scale growth in storage in New South Wales between now and 2035 in similar quantities as outlined in the roadmap.

Results

Broadly speaking the results below are relative to demand which is modelled to increase about 0.5% per year compound. As prices are now expected to be lower demand might be a bit higher.

Prices to fall $15/MWh by 2030, relative to ITK prior case

Some investment bank analysts believe that prices are driven by gas generation and as the gas price recovers so will electricity prices. ITK believes that gas generation has had an important role historically but going forward we think those investment banking analysts are way off course.

By 2030 we expect that relative to our pre-NSW announcement forecasts, the NSW build out will lower flat load prices by around $15/MWh in NSW, South Australia, Victoria and Queensland with the impact coming towards the end of the decade.

Rather than show every state and for all fuels, we show NSW and Victoria flat load prices.

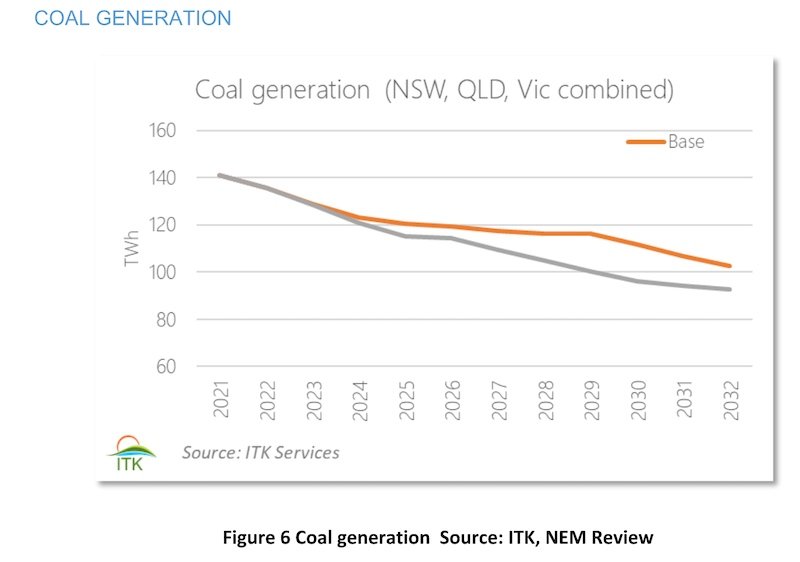

Coal generation

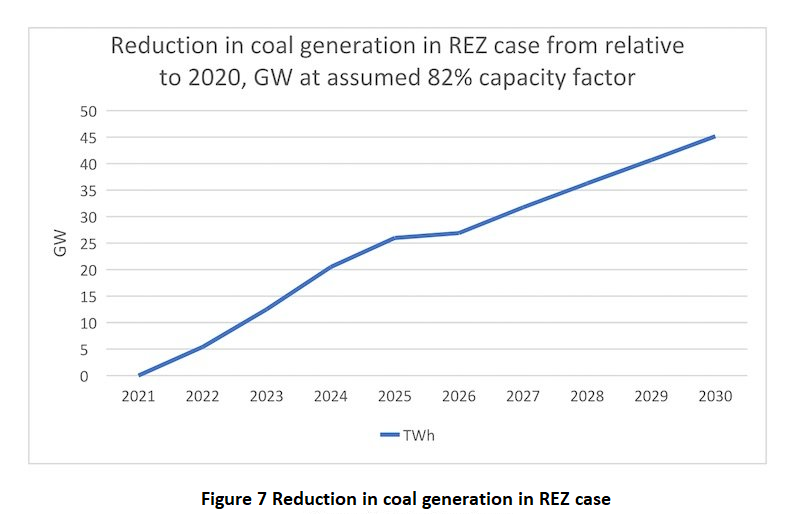

And our next figure shows the REZ case only, in terms of change relative to 2020 in both TWh and also GW assuming an 82% average capacity factor across the NEM for coal generation.

For the REZ case with NSW coal constrained to minimum 2GW we calculate implied energy and power changes as follows:

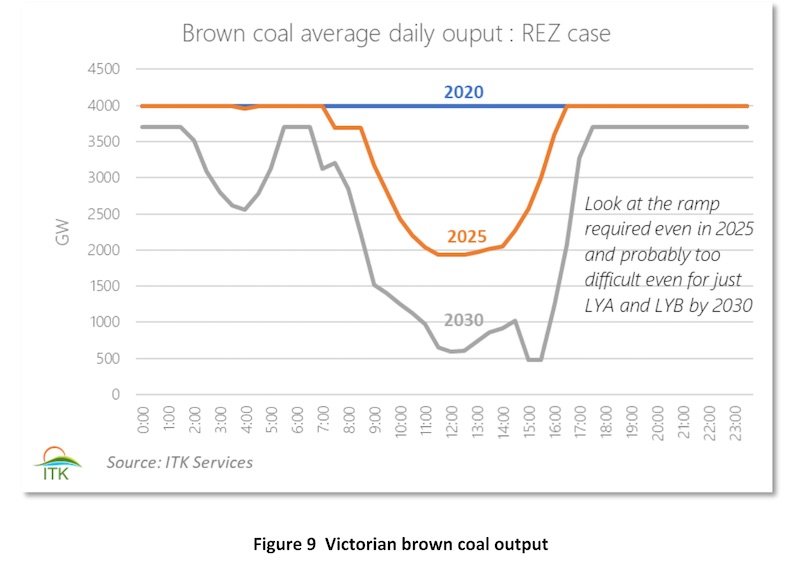

Yallourn has no hope and by 2030 Loy Yang A and Loy Yang B will be in deep trouble

We think that brown coal units at Yallourn are likely to be unviable even by 2025 and even Loy Yang A (LYA) and Loy Yang B (LYB) will struggle by 2030. The reason is not only that prices in Victoria will be in the $40-$50/MWh in the latter half of the decade but mainly that, in our opinion, brown coal generation is inflexible and units cannot be ramped up and down every day. ITK expects brown coal ramping requirement to increase to an unviable level for one generator by 2025 and for all three units by 2030.

We assume that Yallourn has higher marginal and total costs per unit of output than either LYA or LYB and so will be outcompeted. We understand Yallourn units operate on a 5 year campaign schedule. Two units are older and two are better. You can observe using say NEM Review that the older units startup after maintenance at about half the speed of the new units.

Its open to CLP, owners of Yallourn, to close down say 2 units but this would lead to a sharp rise in average costs for the remaining units as most of the power station costs are fixed.

Looking a few years further out we note that LYA and LYB share a common coal supply from the mine at LYA. LYB may well have lower costs than LYA but can’t run without it.

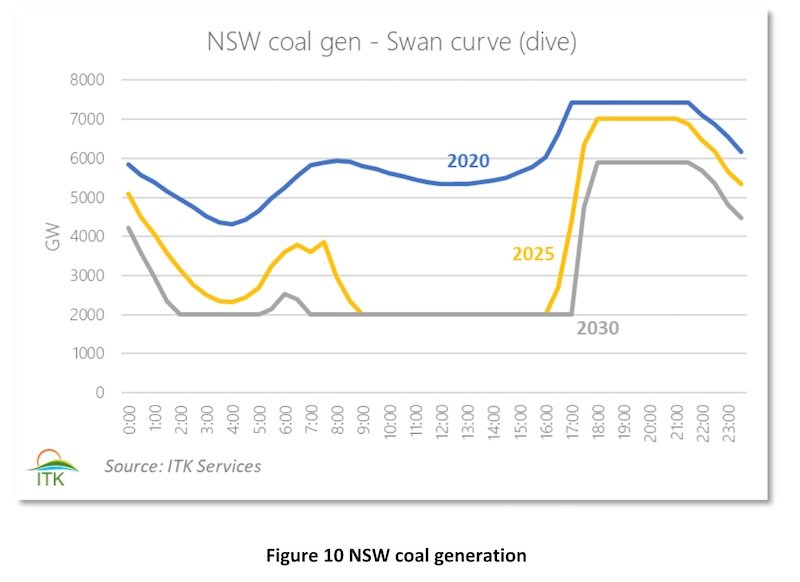

And for coal Generators in NSW

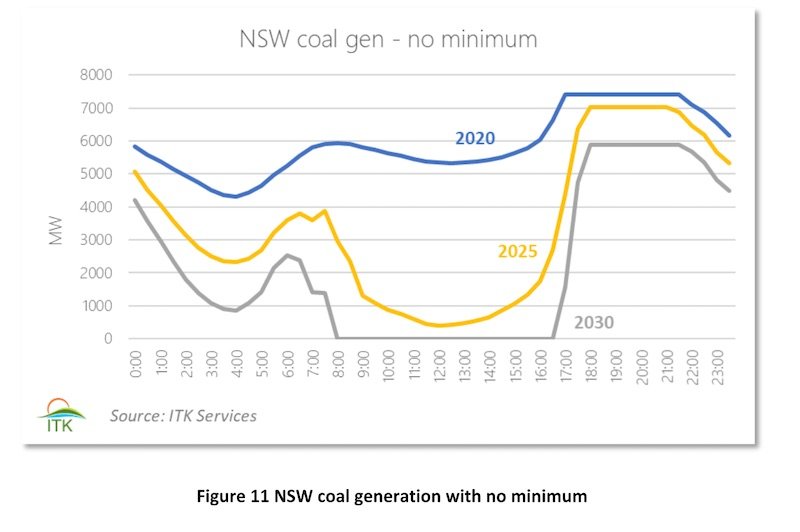

ITK has, for our forecasts, historically constrained minimum coal generation in NSW to 2 GW, compared to a daily average peak over 7GW.

However, for this note we also ran our model with that assumption relaxed, i.e. no “must run” coal and get this result:

If we allow all NSW coal volumes in our model to compete based on cost, rather than bidding in at the market floor, the result is clear: market share is significantly eroded by cheaper thermal generation from both Queensland and Victoria. By 2025 the NSW fleet spends a significant chunk of daylight hours below 1GW, and by 2030 there is no requirement for local coal generation at all between 8am and 4pm.

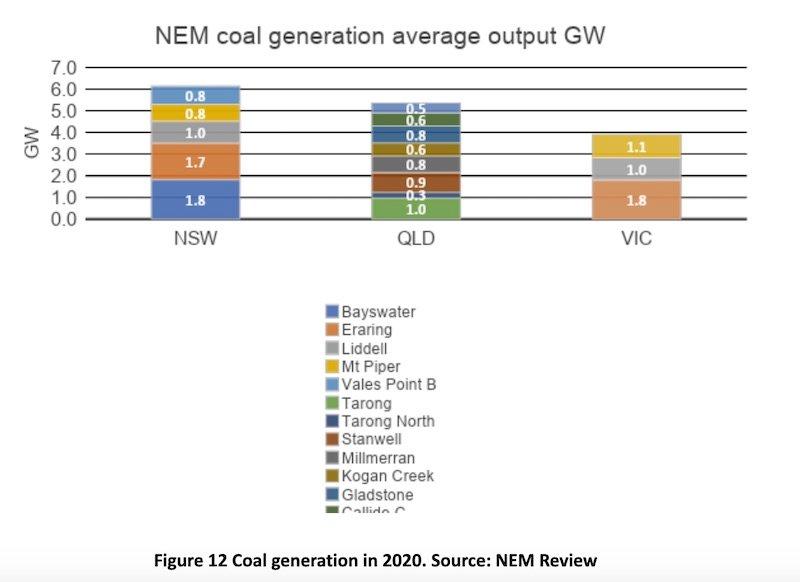

But that won’t happen. The figure below shows average GW of generation. You can see that Bayswater and Eraring alone are more than 2GW. Their owners will protect their market share against losses to Victoria.

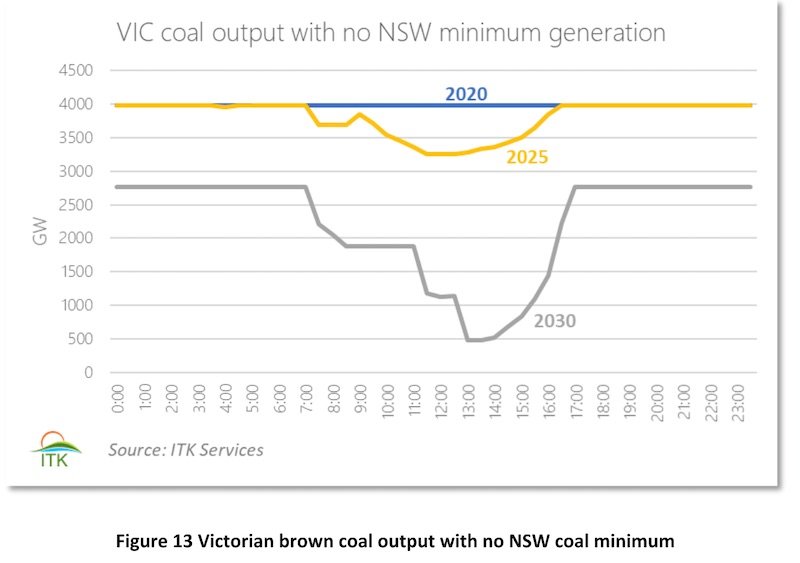

While we expect NSW generators to compete fiercely on price – including continuing to offer major volumes at the market floor – a scenario with no minimum generation output is a positive for brown coal generators in Victoria.

The cost advantage enjoyed by Victorian generators allows them to take market share in New South Wales, dampening the ramp rates required for the evening peak. 2025 looks considerably more palatable for Victorian coal under this scenario, although we still consider the 2030 production profile will place unrealistic stress on the aging brown coal fleet.

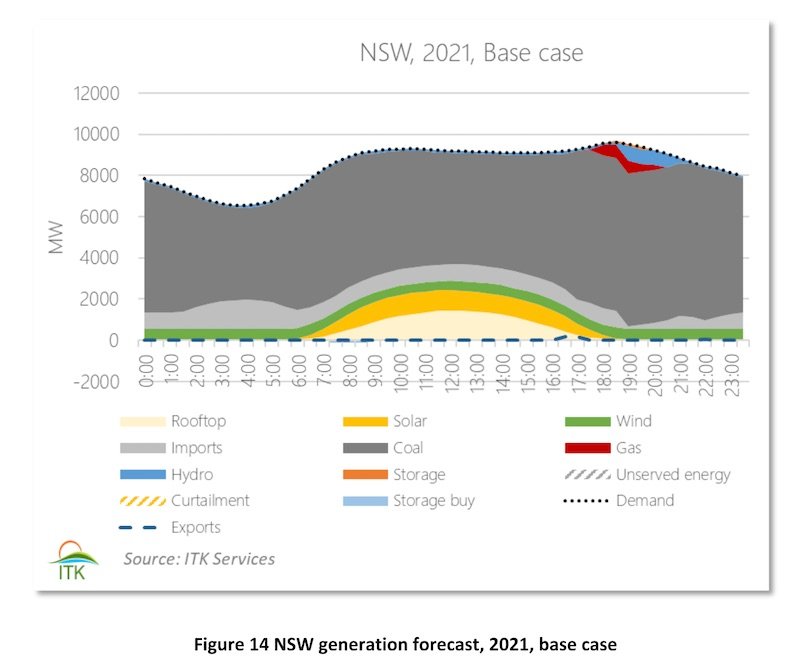

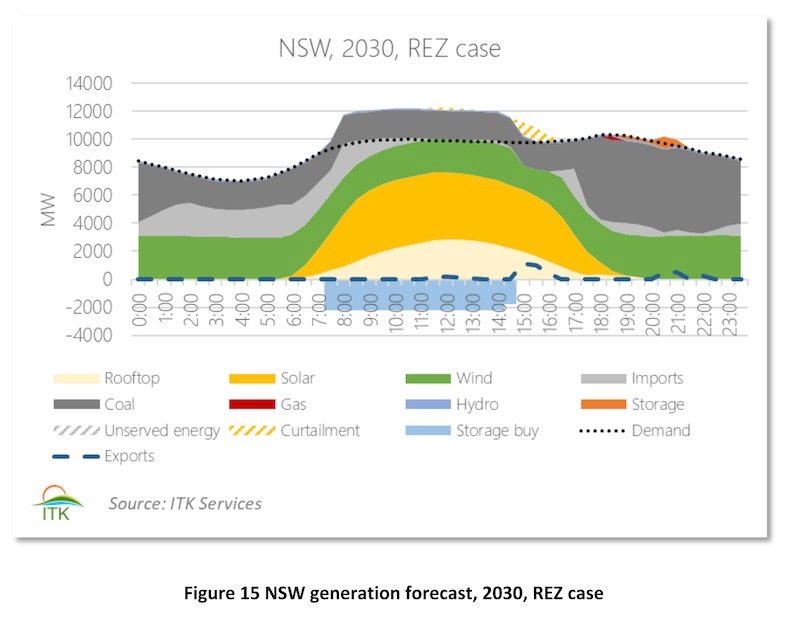

For the sake of completeness the two figures below show the 2020 NSW average daily output by fuel and time of day compared to the NSW REZ case in 2030. Due to our minimum coal assumption there is more spillage than may be necessary.

Solar to require more support than wind

While the focus of this report is the impact on coal generation, we also note some other key implications of the government’s announcement, which we will build upon in future analysis.

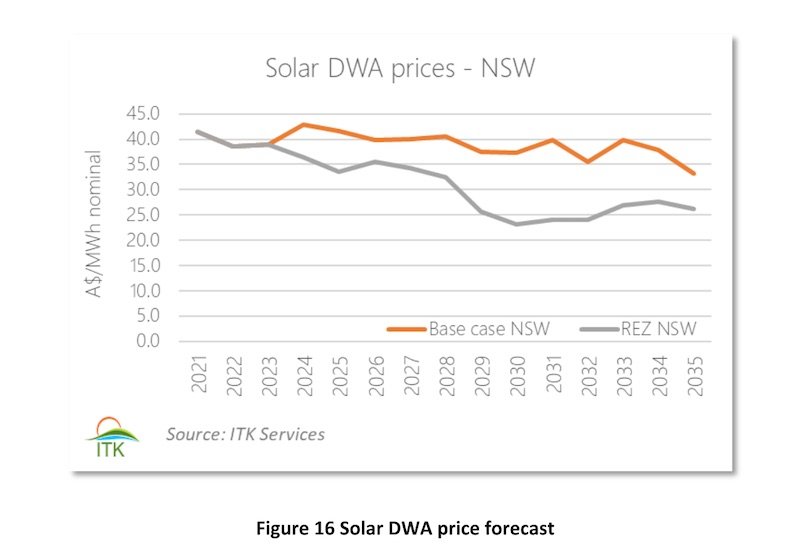

The growth in solar within the two REZ areas has a marked impact on the already low outlook for merchant solar dispatch weighted average prices in New South Wales.

And while average annual wind DWA prices also fall, they remain higher as we expect them to track closer to the flat load average.

We therefore expect the government, via the Consumer Trustee, to make more payments to solar projects under this policy than wind. We do not, of course, know the likely bids developers will make in the reverse auction, but we anticipate they will likely be close to the project breakeven price (the price required to cover costs and earn a return on capital).

There is little scope for a lucrative merchant tail under our forecasts, so given our view of current utility solar costs, we would not be surprised to see a higher proportion of solar developers putting the option to receive the minimum revenue payment.

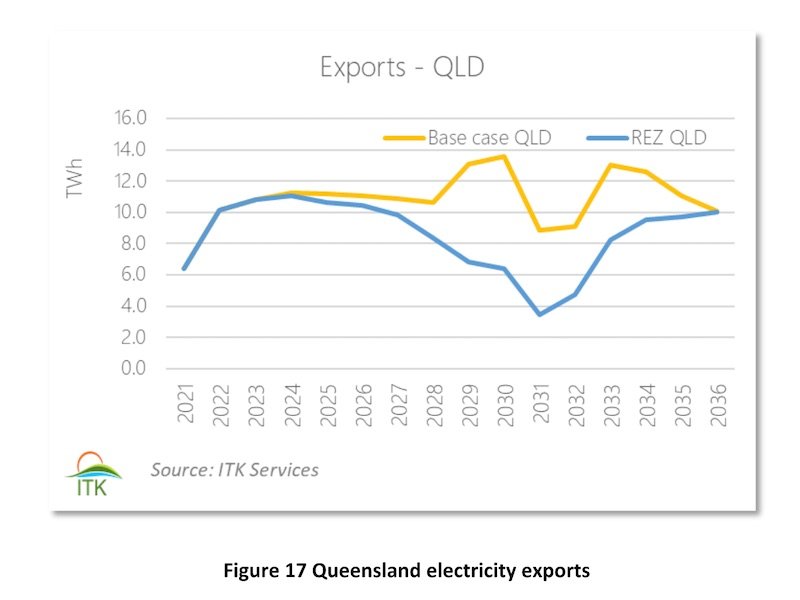

Importers take a haircut

Not surprisingly, introducing a higher proportion of zero marginal cost supply into New South Wales – the biggest market in the NEM – reduces the average requirement for imports. This hits South Australia to some extent given our expectation of strong VRE exports into New South Wales following the completion of the EnergyConnect interconnector.

The impact on Victoria is greater, as most imports to 2035 are likely to be from brown coal generators, which have higher costs than renewables. But the greatest shock is to Queensland, as black coal generation exports get squeezed out over the medium term.

We expect some TNSPs may need to revisit the financial modelling for interconnector build and expansion proposals in light of NSW’s roadmap.

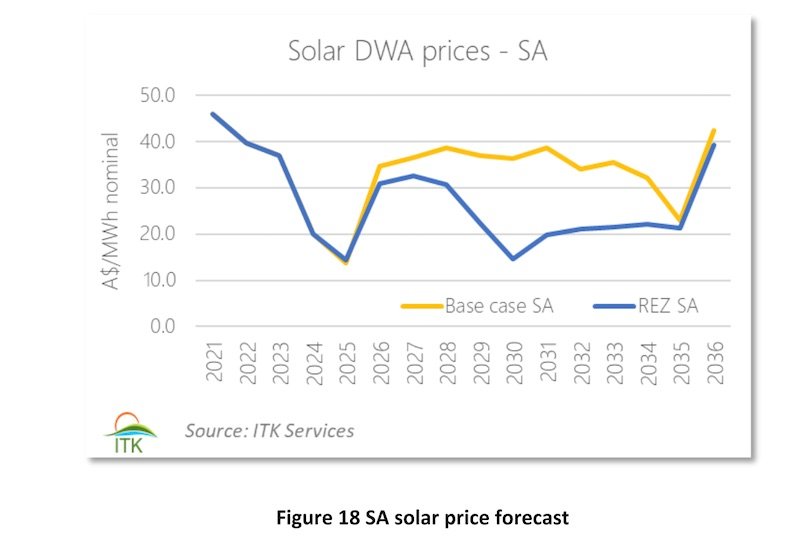

South Australia

In fact South Australia bears a number of impacts from the New South Wales strategy. One that jumps out to us the most is solar pricing in the state. If Project EnergyConnect eventually gets off the ground, South Australian prices will be far more closely driven by New South Wales. With prices coming down in New South Wales as a result of massive VRE growth and cut-throat competition between thermal generators, South Australian prices also get pulled down.

This is most true for solar prices, as South Australian operators will get a much smaller benefit from New South Wales coal generators sitting at the margin.

It won’t be lost on South Australian market participants that solar projects in the state face the same reduction in prices, but without the financial safety net.

——————————————–

About our Guest Author

|

David Leitch is Principal at ITK Services.

David has been a client of ours (and a fan of NEMreview) since 2007. David has been a long-time contributor of analysis over on RenewEconomy, very occasionally contributes to WattClarity! David also provided valued contribution towards our GRC2018. David has 33 years experience in investment banking research at major investment banks in Australia. He was consistently rated in top 3 for utility analysis 2006-2016. You can find David on LinkedIn here. |

Interesting article.

Figure 15 shows 16GWh of Storage Buy each day. Is this plan using Snowy 2.0 – It would be a very expensive Battery!

Figures 14 and 15: At 18:00 both 2021 and 2030 seem to require 6GW of coal. I am misunderstanding something?

The storage buy is effectively spilled energy for the most part. Its available for storage but in the end most isn’t used.