One of Paul McArdle’s Twitter connections (no relation to your guest author!) posed this question about the $14,000/MWh Queensland price spike last Friday, in dispatch interval (DI) 10:35am:

In this first of what will be an ongoing series of event reviews in the NEM, I’ll do my best to give a quick(ish) reply.

But as this is a first post, I’ll give both a quick and a more extended answer, illustrating one approach to reviewing market events like this in more detail. Don’t worry, future posts will be considerably shorter!

The Quick Version

Just before the spike, although there were no concrete forecasts of such extreme prices in Queensland, there were a number of warning signals: there had been a couple of earlier jabs to just over $1,400/MWh, demands were running above forecast, interconnector flows from NSW into Queensland were constrained, and overall we have seen a volatile spot market in Queensland this summer reflecting a very “thin” generation bidstack (see Paul’s forensic WattClarity post on “Sizzling Saturday” 14th of January for a wealth of detail on this).

At DI 10:35, this all converged to a smallish rise in 5 minute Queensland demand leading to a very large jump in dispatch price from $98.94/MWh to $14,000/MWh, as lower price generation offers were fully utilised and AEMO had to dispatch very high priced Queensland generation offers to meet demand – but this did not mean that Queensland was anywhere near running out of generation capacity – just that a relatively large amount of that capacity was offered only at very high prices.

And that “negative residue” on the NSW-Qld interconnector mentioned in Mitch’s tweet? Well that reflects behaviour immediately after the spike. DI 10:35 is the first 5 minute dispatch interval in the half hour Trading (Settlement) Interval covering 10:30 – 11:00. Financial settlement prices in the NEM are the half hourly average of the six 5-minute dispatch prices in each half hour, so a $14,000 price in the first DI guarantees a settlement price of at least $1,500/MWh(1). All generation dispatched anytime during the half hour earns that settlement price, so generators had a strong financial incentive to increase volumes in the next 25 minutes(2), by offering more capacity at lower prices. This is an example of the much discussed “5/30” issue, covered previously here on WattClarity.

In the event, that’s what happened – Queensland generators rebid to lower price bands, increasing local generation and reversing flows on the QNI and DirectLink interconnectors in the rest of the half hour, resulting in an net southwards flow of energy. But that single $14,000/MWh price in Queensland for the first 5 minutes meant that for 10:30-11:00 as a whole, the Queensland and NSW half hourly settlement prices – on which interconnector residue payments are also calculated, another artefact of the 5/30 issue – were counter to the net flow direction, with power flowing from the high price ($2,353.04/MWh) Queensland region into the low price ($49.65/MWh) NSW region. Effectively, the NEM “bought” high price Queensland energy and “sold” it for low prices in NSW. “Negative Residue” is just a technical term for “losing money” on these counter price interconnector flows!

Footnotes

(1) That $1,500/MWh minimum would only occur if the next 5 DI prices were all at the market floor price of negative $1,000/MWh. In practice we’d usually expect a half hourly average of over $2,000/MWh.

(2) And price-responsive loads would similarly have a strong incentive to reduce their demand over the rest of the half-hour

The Extended Answer

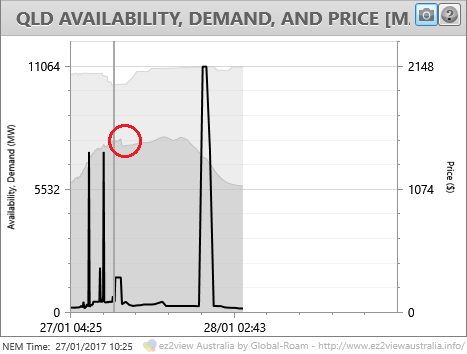

Let’s start by reviewing the market conditions and outlook a short time beforehand, using the Time Travel function in global-roam’s ez2view market analysis tool. I’ve wound the clock back to DI 10:25am. Here are the graphical trends – actuals and pre-dispatch forecasts – for price, demand, and generator availability as seen in ez2view:

We can see there were a couple of earlier five minute spikes to around $1,200/MWh (price is the dark line on this chart), however the immediate outlook for dispatch prices doesn’t show anything much over $300/MWh. Generation availability (the lighter grey area) is comfortably above demand. But one thing to note here is the apparent drop in demand (the darker grey area series) about one hour ahead, which I’ve circled on the chart.

This point is where AEMO’s on-the-day demand forecasts cut over from “P5” (5 minute) to “P30” (half hourly) granularity, and are produced by two slightly different processes. The fact that the P5 version is running significantly above the P30 (by about 200MW) is a tell-tale sign that actual demands are turning out to be higher than forecast earlier in the day. This is one early warning sign that there could be price risk on the upside.

(No space to go further into this here, but ez2view’s Forecast Convergence widget is a very useful tool for looking more more deeply into how forecasts and actuals for key measures like price and demand evolved for any given day or period.)

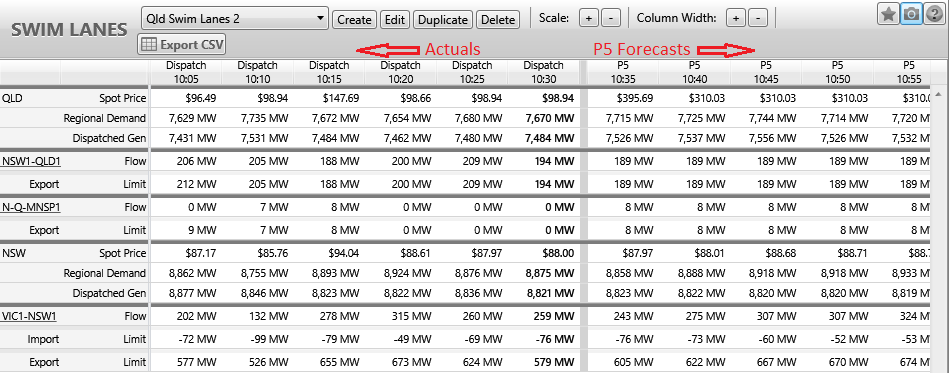

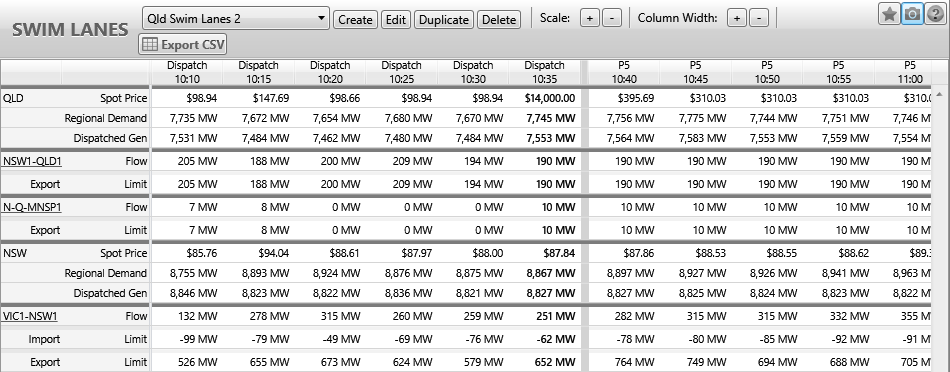

Stepping one interval forward in ez2view to DI 10:30, not much changes. This time I’ll show the numerical values for price, demand and a few other items using ez2view’s Swim Lanes widget, a useful and flexible tool for viewing a wide variety of NEM data in tabular format:

The first few rows here give a quick overview of what’s happening in the Queensland region and the two interconnectors linking it to NSW:

- 5 minute actual prices sitting around the $100/MWh mark but forecast to go into the $300/MWh range from DI 10:35 onwards,

- actual demands bumping around the mid 7600MW – low 7700MW range and forecast to stay above 7700 MW in the near term, and

- “Dispatched Generation” – ie the amount of Queensland generation dispatched by AEMO – moving out of the mid 7400 MW range and into the low 7500 MW range

The reason Dispatched Generation is less than demand is explained by the next couple of bands in the table, showing the flows and limits on the QNI (“NSW1-QLD1”) and DirectLink (“N-Q-MNSP1”) interconnectors. Around 200 MW of power is flowing from NSW into Queensland on these links, but the fact that flows are up at their respective limit values means that both links are constrained. Any further increases in demand can only be met from local generation, and Queensland prices are liable to separate from those in NSW and the rest of the NEM. This is another warning sign for potential price volatility in Queensland.

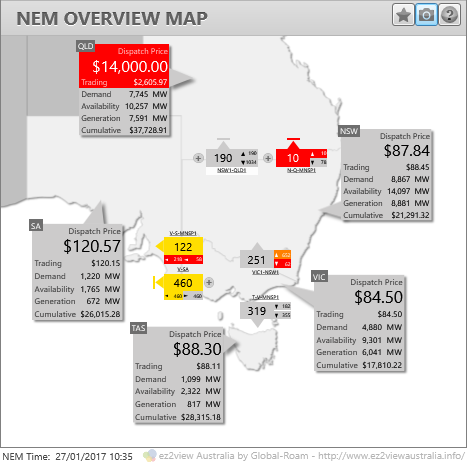

Rolling forward to DI 10:35 and – bang (shown on ez2view’s NEM Overview Map):

The Swim Lanes view for 10:35 shows that 5 minute scheduled demand, 7745MW, has actually jumped a little bit higher than was forecast in the previous P5 run (7715 MW, per the earlier Swim Lanes screenshot above)

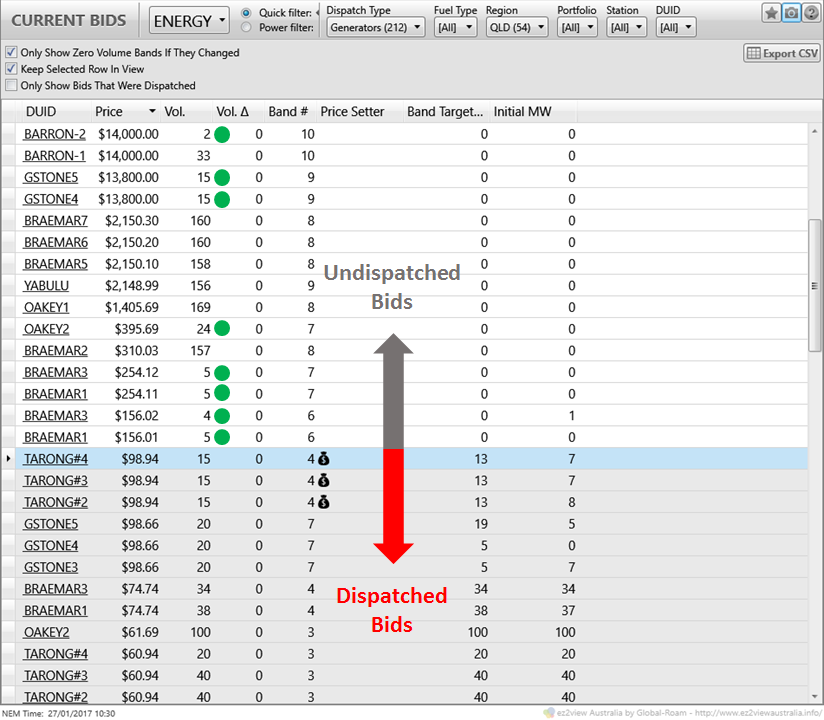

But why did a relatively small move in demand lead to such a large change in the Queensland price? To conclusively answer this we need to open up ez2view’s Current Bids widget and see what the Queensland generation bidstack was showing (note that we can only access this bid data next day, it is not published live):

Here are the bids for DI 10:30:

I’ve sorted the bids in descending price order and focussed on those centered around the current dispatch price.

Next to the price column for each bid, the table shows the volume offered in that price band by each generating unit, while the second last column to the right shows how much of that volume was called on (the “Band Target”) by AEMO’s NEM Dispatch Engine (“NEMDE”). Higher priced bids with a band target of 0 MW are not dispatched.

For this DI, Tarong units are setting price at $98.94/MWh, being the last bids dispatched to meet scheduled demand.

We can also see that there are not all that many bids at prices between $100/MWh and $13,800/MWh.Those intervening bids are all from gas turbine units at Braemar A (units 1-3), Braemar B (units 5-7), Oakey, and Yabulu (Townsville). And while there seem to be plenty of MW offered in those bands and able to supply increases in Queensland demand, not all of these units are started up and online – only those that I’ve indicated with the green circles (ez2view’s Region Schematic widget for Queensland readily shows which units were running, but that’s omitted here for space reasons). There is thus very little spare capacity offered at prices below $13,800/MWh on units which are actually running. The offline units will be ready to start when called on, but gas turbines don’t start producing power instantly and generally need 5 – 10 minutes to run through their startup sequence.

(One reason those GTs are not already running may be the high market price of gas – around $10/GJ – and at prices below $100/MWh or even a little higher, those units would be running at a loss to stay online.)

So if demand increases by not too much in the next DI, NEMDE will need to dispatch what extra MW are bid from those running GTs, but will pretty quickly run into the very high price bands at the upper end of the bidstack. Which is exactly what transpired in DI 10:35, setting the price up at $14,000/MWh (there were some minor changes in bids between the two intervals but they don’t materially change the picture, hence I’ve omitted the 10:35 bidstack view).

Subsequent Events

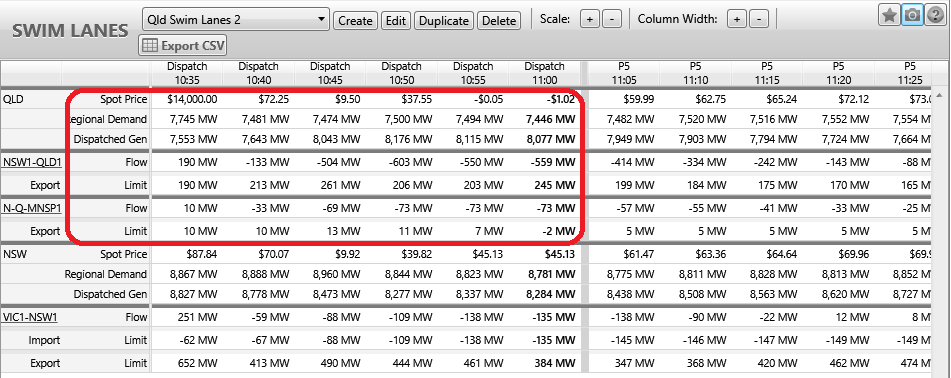

As explained in the quick answer above, the very high price in the first 5 minute dispatch interval and the “5/30” effect of 30 minute financial settlement prices being the simple average of this and the next five dispatch prices, strongly incentivise generators to rebid, increasing volumes in lower price bands to increase dispatch, and price-sensitive loads to reduce demand. And to limit the length of this post, we can see how all this played out over the remainder of the half hour in this swim lanes view:

We see:

- Spot prices plunging to low levels as generators rebid volumes to lower prices

- Demand falling by nearly 300 MW, almost certainly due to price-responsive loads reducing

- Dispatched Generation increasing by over 500 MW (including startups at a number of the offline gas turbine units mentioned above), and

- Interconnector flows turning around from 200 MW of import to over 600 MW of export from Queensland to NSW, producing a significant net southward flow for the half hour, even though the average Queensland price for the half hour ($2,353.04/MWh) was – thanks to that single $14,000/MWh spike – well above the NSW half hourly average ($49.65/MWh). And hence the negative settlement residues referred to in Mitch’s tweet.

A lot of activity prompted by one five-minute price spike!

|

Allan O’Neil has worked in Australia’s wholesale energy markets since their creation in the mid-1990’s, in trading, risk management, forecasting and analytical roles with major NEM electricity and gas retail and generation companies.

He is now an independent energy markets consultant, working with clients on projects across a spectrum of wholesale, retail, electricity and gas issues. You can view Allan’s LinkedIn profile here. Allan will be regularly reviewing market events here on WattClarity. Allan has also begun providing an on-site educational service covering how spot prices are set in the NEM, and other important aspects of the physical electricity market – further details here. |

Leave a comment