Editor’s Note – Matt has adapted this article from a keynote presentation he gave at the Energy Storage Summit in Sydney on Tuesday 18th March 2025.

It’s well known that the NEM is currently experiencing a wave of investment in Battery Energy Storage Systems (BESS). You’ve probably seen a bar chart or two showing the NEM’s installed BESS capacity moving ‘up-and-to-the-right’ in the years ahead. But behind the basic capacity growth data lies an untold story about the changing nature of competition and trading in the NEM.

As more BESS capacity gets added to the market, we are seeing a diversification of the market participants in control of that capacity and a diversification of trading strategies and objectives across the BESS fleet. This should increase overall competition and reduce the potential market power of any one participant.

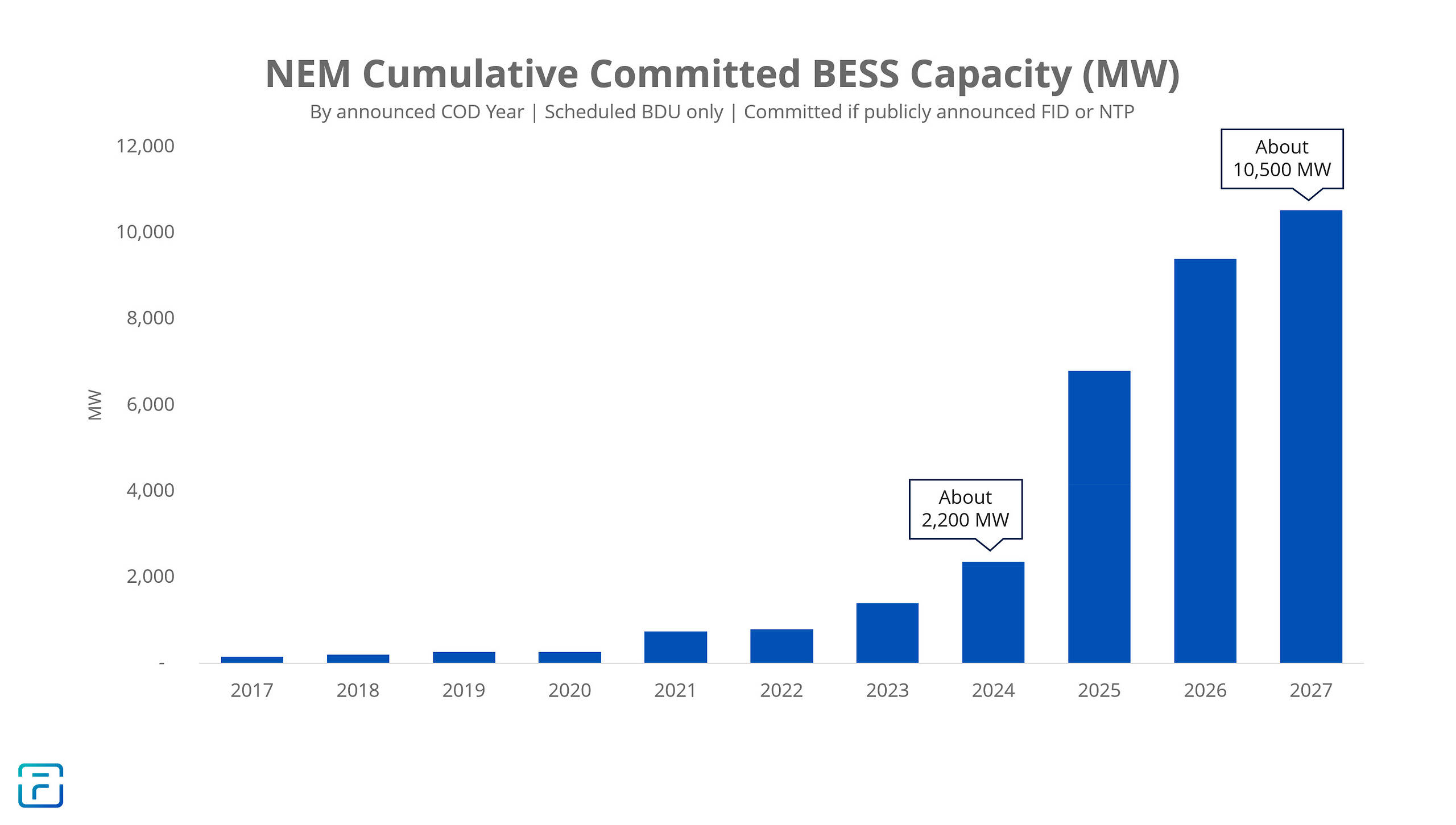

Accelerating BESS capacity in the NEM

BESS capacity in the NEM is set to grow rapidly over the next three years.

The chart below shows the total BESS capacity that is ‘committed’—meaning it is either already operational or has been publicly announced to have reached financial close, given notice to proceed to its suppliers, and commenced construction.

Note: Figures based on Fluence’s analysis of MMS data and public announcements, as of the 15th March 2025. The “COD Year” refers to the expected/announced year of the ‘commercial operation date’. This typically refers to the date the BESS completes its commissioning programme and commences unrestricted trading in all wholesale market services. Therefore, there is little uncertainty around the BESS projects in this dataset, and no pipeline projects (that might not go ahead) are included. This data only reflects large-scale standalone BESS (i.e. Standalone Scheduled BDU > 5 MW), it doesn’t seek to capture small BESS projects or hybrid BESS projects.

The data reveals that:

- 2025 is looking to be a historic year, where the NEM will approximately triple its current operational BESS capacity

- By the end of 2027, the NEM should have at least quintupled its BESS capacity from today. It is easy to imagine another 1-2 GW of projects reaching financial close before the end of 2025 and commissioning before the end of 2027, so the 2027 bar should grow higher still.

- Therefore, 2027 could be the year that NEM BESS capacity eclipses gas generation capacity (about 13 GW).

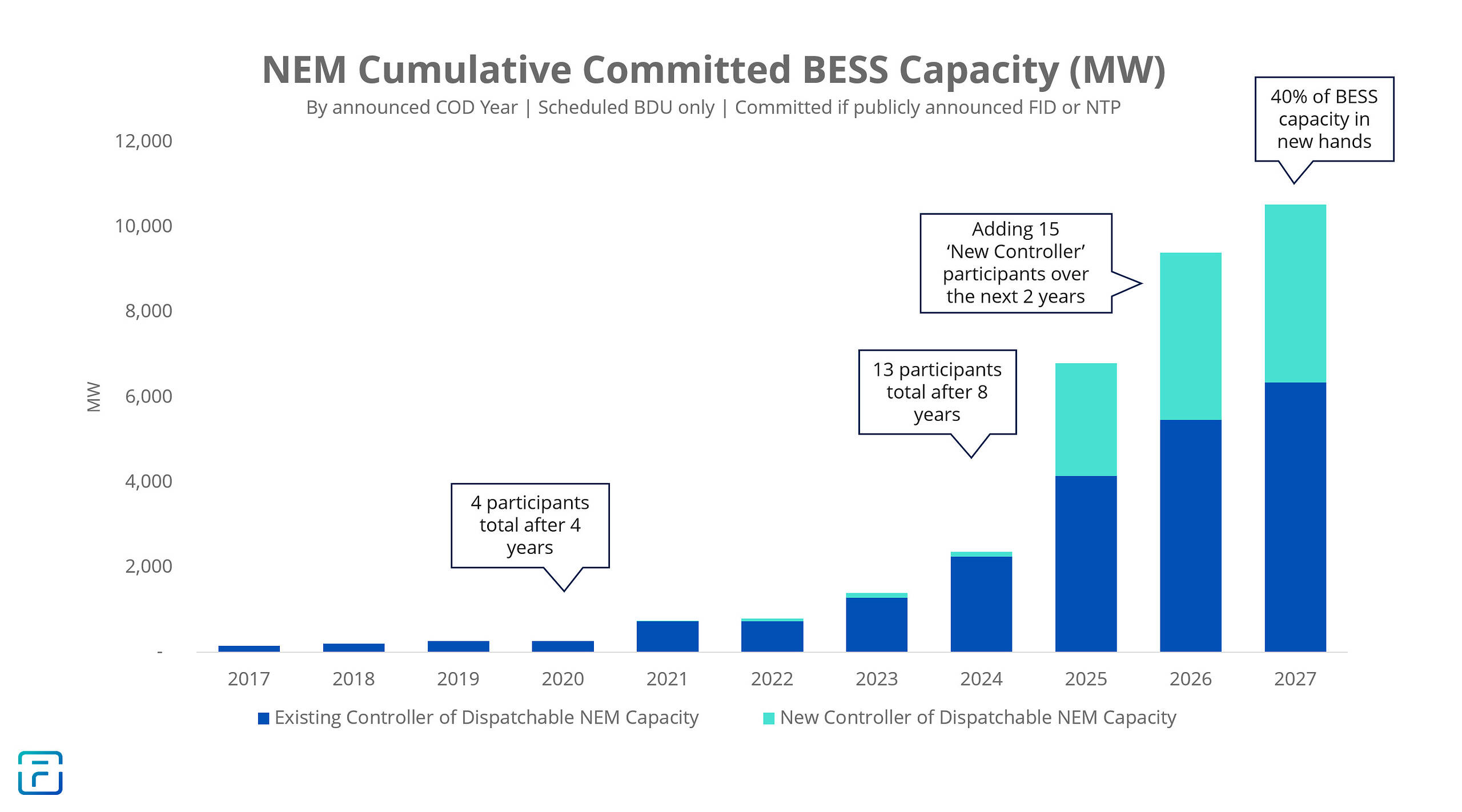

Who is in control of these BESS?

To identify who is trading and controlling this growing fleet of BESS, it’s important to consider which market participant has the trading rights and will be controlling and bidding the BESS into the wholesale markets. In this context, the owner of the BESS is less relevant.

Therefore, the BESS capacity chart below has been broken into two categories of controllers:

- Existing controllers of dispatchable capacity – market participants with prior experience bidding scheduled units into the market (prior to 2021).

- New controllers of dispatchable capacity – market participants who have no prior experience bidding a scheduled unit.

Scheduled units are dispatchable resources that bid on-demand capacity, i.e. coal, gas, hydro, storage > 5 MW, and demand response. Scheduled units are fundamentally distinct from semi-scheduled units (i.e. wind and solar farms) and have more compliance obligations in the bidding and dispatch process.

Note: Figures based on Fluence’s analysis of MMS data.

Breaking out the data this way reveals several key insights:

- Through 2020, only four market participants had experience bidding BESS (NeoEn, EnergyAustralia, AGL, Iberdrola)

- Over the subsequent few years, a handful of new participants entered the market, but by the end of 2024, the vast majority of BESS capacity (95%) was still being traded by existing participants. Many of these were so-called gentailers with complex portfolios.

- But in the next two years, the number of new participants is going to expand significantly, and the NEM will add (at least) 15 ‘new’ participants to the mix. By 2027, around 40% of the BESS capacity will be controlled by new players.

- However, existing participants will continue to add additional BESS to their portfolios in the years ahead, and some will gain control of their first BESS (like Origin Energy). It is also possible that a new participant might sign a physical offtake agreement with an existing participant, thereby tolling away the trading rights and resulting in some of the green capacity in the chart converting to blue.

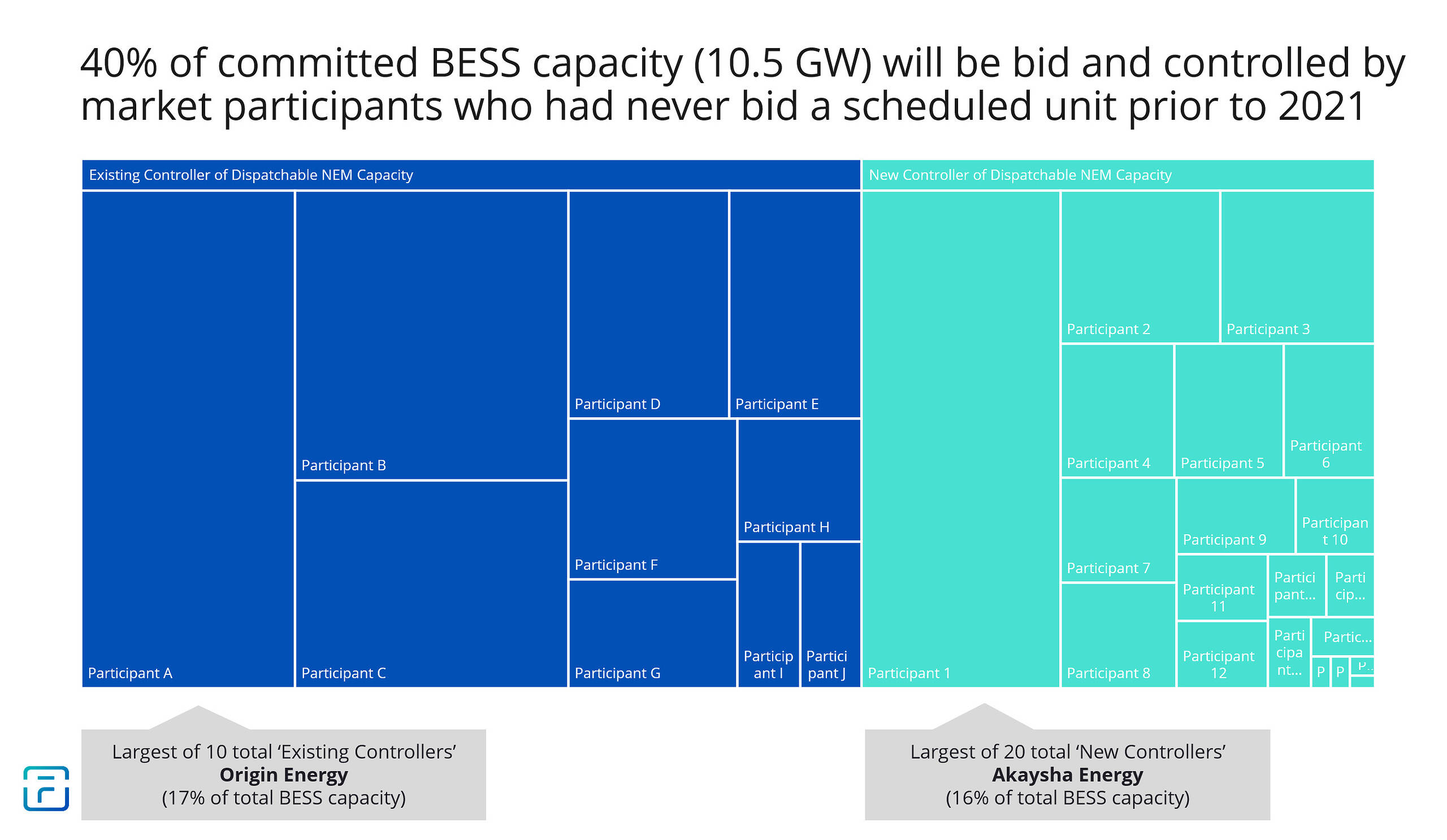

A diversifying mix of market participants

When we drill into the data to visualise the relative capacity controlled by each market participant, an even clearer picture emerges: the participant mix is rapidly diversifying, and new entrants are gaining market share. The treemap below shows that by the end of 2027, the two largest BESS traders by market share will likely be Origin Energy and Akaysha Energy, neither of whom controls a fully operational BESS today. But with the two largest participants controlling 17% and 16% market share respectively, it seems unlikely that any single participant will have a dominant market share or the ability to exercise undue market power based on their BESS capacity.

This increase in the number and diversity of market participants will potentially have impacts both on the market and on the new participants themselves.

Market impacts: Looking back to the first few decades of the NEM, the majority of the dispatchable capacity was controlled by just a handful of large, integrated businesses. That was also the story of the first eight years of BESS trading in the NEM. But 2025 is the year where that story will start to change.

As the above treemap shows, new BESS capacity will be controlled by a diverse mix of market participants, including local IPPs, overseas investors, pure-play BESS platforms, infrastructure funds investors, gentailers, retailers, and more. It will also include BESS projects with diverse contractual arrangements: some with network support contracts, some with merchant priorities, some managing virtual toll contracts or capacity swaps they’ve sold, some defending cap contracts, and some supporting retail portfolio positions. The BESS fleet is going to be trading with increasingly diverse objectives in mind. As a result, the market will likely see an increase in competition, a mitigation of market power, and a diversity of trading objectives.

Participant impacts: The new participants are entering a new world that will require them to evolve their trading capabilities. BESS represent a new asset class and trading a BESS requires a big step up in capabilities from trading a wind or solar farm. These new participants are going to require new IT systems, new tools, new processes, and new capabilities to trade their BESS effectively and to achieve the goals set out in their business cases.

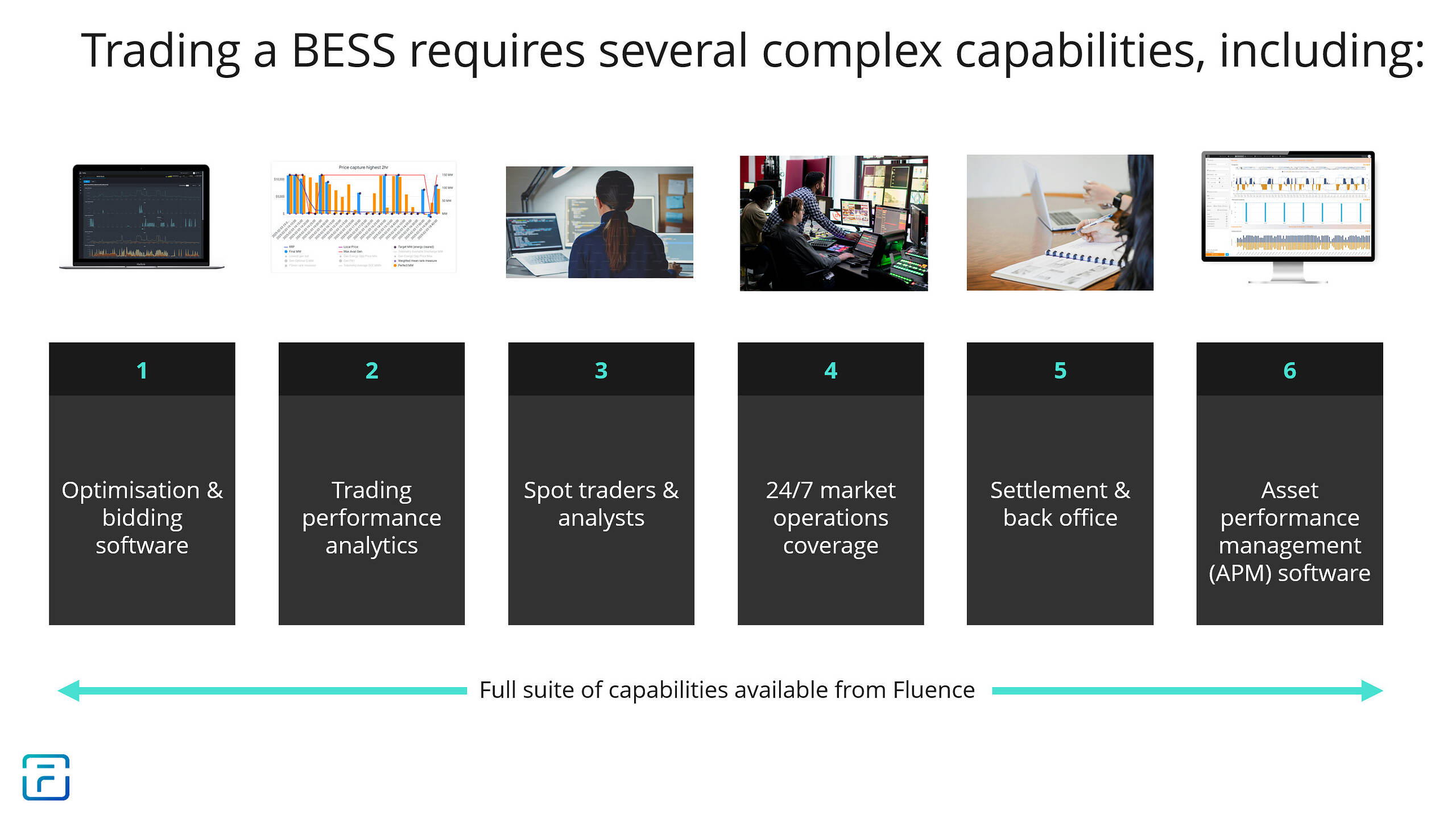

What is needed to trade a BESS in the NEM?

For BESS in the NEM, it is now widely recognised that using some sort of automated bid calculation and submission tool is essential to ensure bids are made compliantly and the BESS’ limited energy is utilised efficiently. At Fluence we help dozens of market participants optimise and execute their trading strategies through our Fluence MosaicTM software, an algorithmic bid optimisation tool for wind, solar, and BESS assets. Mosaic is a trading tool used by many of the NEM’s most significant BESS assets and semi-scheduled wind & solar generators. Market participants use Mosaic to operationalise and execute their trading strategies, including management of their financial contracts, OEM warranties, and risk management preferences.

A diversity of BESS participants in the NEM use Mosaic. On one end of the spectrum are small non-scheduled BESS such as Gransolar’s Longwarry BESS project. On the other end of the spectrum, larger BESS traders and assts rely on Mosaic, including Akaysha Energy at their Waratah Super Battery project, the largest BESS in the NEM. At Waratah, Mosaic helps Akaysha manage a key system integrity protection scheme (SIPS) contract while simultaneously trading a portion of the BESS on a merchant basis.

However, bid optimisation is only one of several key, highly complex capabilities that every market participant needs to trade a BESS compliantly and effectively. We have outlined some of these capabilities in the diagram below.

Fluence recognises the diversity of BESS participants in the NEM and offers the full suite of capabilities that participants need to trade a BESS, which can be tailored to individual customer needs, depending on their existing and future internal capabilities. For participants who want more than bid optimisation software, Fluence can now provide a range of Trading Services, where our trading team helps participants oversee their BESS trading and refine their trading strategies.

We often get asked about the role of automation vs human oversight in the BESS trading process. Every BESS project we’re working with uses a combination of algorithmic software automation combined with human oversight to trade in the market. Our experience shows that relying solely on one, without the other does not provide effective results.

The software does the heavy lifting on keeping track of all the fast-changing numbers (changing price forecasts, changing physical plant limits, changing FCAS trapeziums, forward-planning state-of-energy, etc). Human traders keep an eye on the forecasts and the market, review outcomes, tune input settings, apply a portfolio lens, and tune strategies including risk management preferences. Mosaic allows traders to apply any number of layered interventions to the native algorithmic trading strategy, everything from giving the algorithms a gentle nudge, to making a hard override and dictating specific bid prices and dispatch outcomes.

One thing we’ve learned over the years is that being good at BESS trading in the NEM requires a commitment to reviewing trading outcomes, gleaning lessons learned, and feeding those lessons back into the software to improve future outcomes. BESS and their bidding systems ingest a lot of data, and create a lot of data, and it is important to have local market trading experts working closely in collaboration with software developers, to achieve the best trading outcomes.

What to watch for in the years ahead

As the mix of market participants controlling BESS in the NEM grows and diversifies, and as the BESS fleet’s trading objectives become more complex, the NEM will see increased competition for dispatchable capacity and a diffusion of market power. In this rapidly evolving market environment, the teams and the systems supporting these BESS assets with bidding algorithms, trading analytics, and market operations must evolve just as dynamically. At Fluence, we are looking forward to helping our market participant customers stay on the cutting edge and achieve their trading objectives in the NEM of the future.

About our Guest Author

|

Matt Grover is the Director of Energy Markets at Fluence. Matt’s team works to develop and deliver Fluence’s algorithmic optimisation & bidding software tools, which are used by a significant portion of the NEM’s grid scale BESS and renewable generation fleet. Matt has more than a decade of experience in NEM market operations, across both the supply and demand sides of the market.

You can find Matt on LinkedIn here. |

Are we talking 13GW or GWh

I would imagine that it is discharge capacity.

It is going to be a very complex market to model in terms of estimating how much energy a particular battery might have left in storage, and how much capacity there is in the transmission network connecting these BESS.

I don’t believe there will be that much more competition in the evening peak market by 2027 and certainly not 2025. Fossil gas and hydro are still going to set the price during much of the evening peak, even while fossil gas use drops significantly. A major problem is the transmission networks, not just between states/regions, but within states/regions. We will increasingly see cases where there is capacity and energy available, but the transmission network is operating below its rated capacity, so these batteries can only have limited impact.

SA hasn’t seen as much benefit as should have from the additional BESS in the last 12 months due to a lack of competition.

As per Craig’s comment, perhaps a region by region breakdown of control would be more relevant in considering pricing?

Have they considered a possibility of being able to feed into the grid from under-utitilised home battery systems?

Say I install a 20kW home battery while my kids are still living at home and staying up to 1am playing their PCs and running aircon, etc, but after they’re moved out, all that battery capacity would simply not be needed. Is there any way to tie that back into grid export?